Running a startup has its fair share of responsibilities.

From building and launching a product to business development, the founding team has to wear multiple hats. But they cannot overlook the fundamentals of accounting and the role it plays, especially for early stage startups. We're experienced finance leaders with over two decades of expertise in steering and expanding technology companies. Pooling our collective know-how, we're dedicated to paying it forward by supporting the next wave of startups.

We have broken down our Accounting 101 guide ( OPERATOR model ) that every founder needs to know below

Table of Contents

O : Organization Structure

Before you even launch, you need to have the right organizational structure completed. Choosing the appropriate business entity affects your taxation, how you compensate yourself, your potential business liability, and other critical aspects.

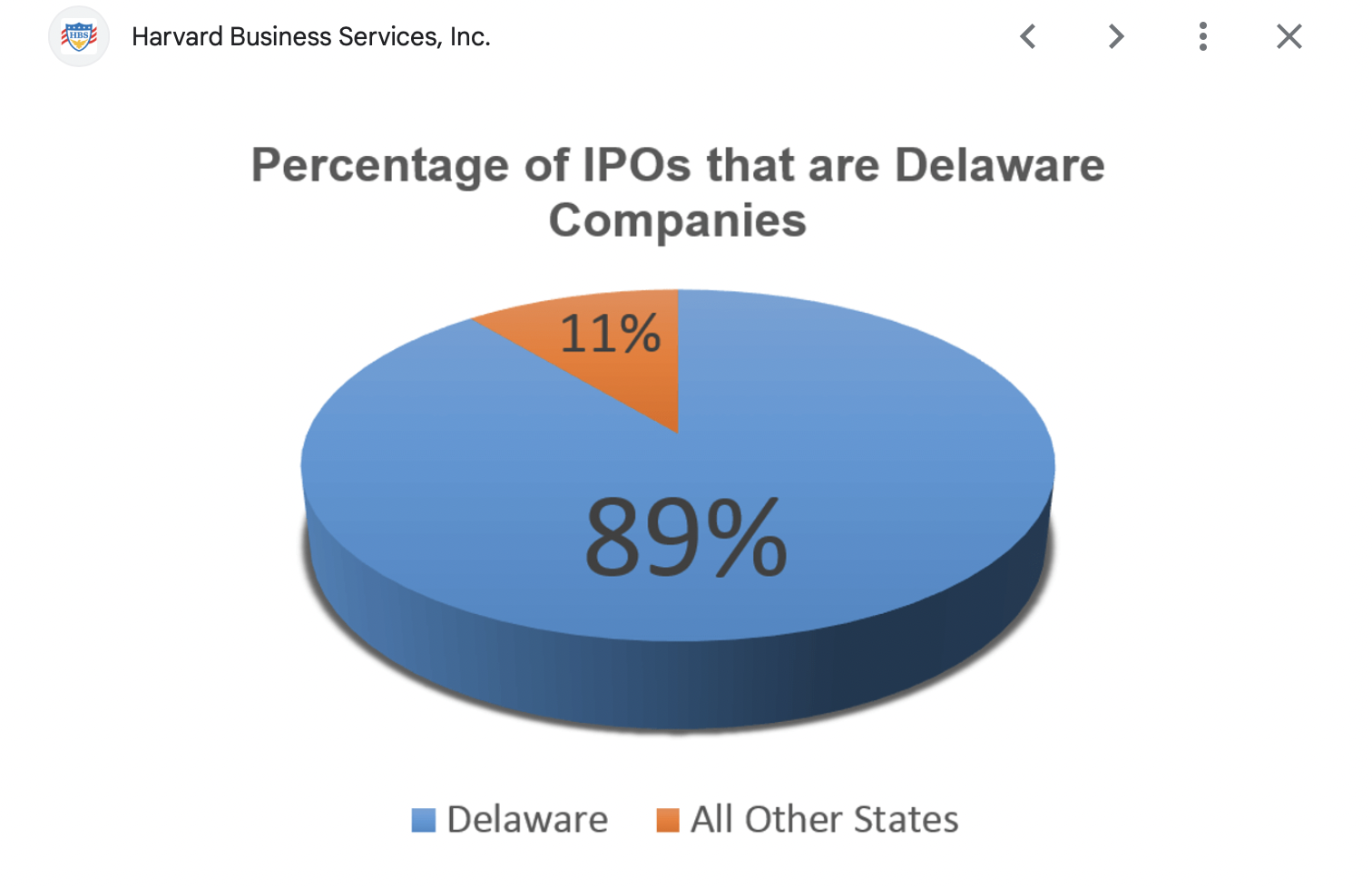

We recommend a Delaware C Corporation due to its advantageous nature for startups.

P : Payroll/Employees

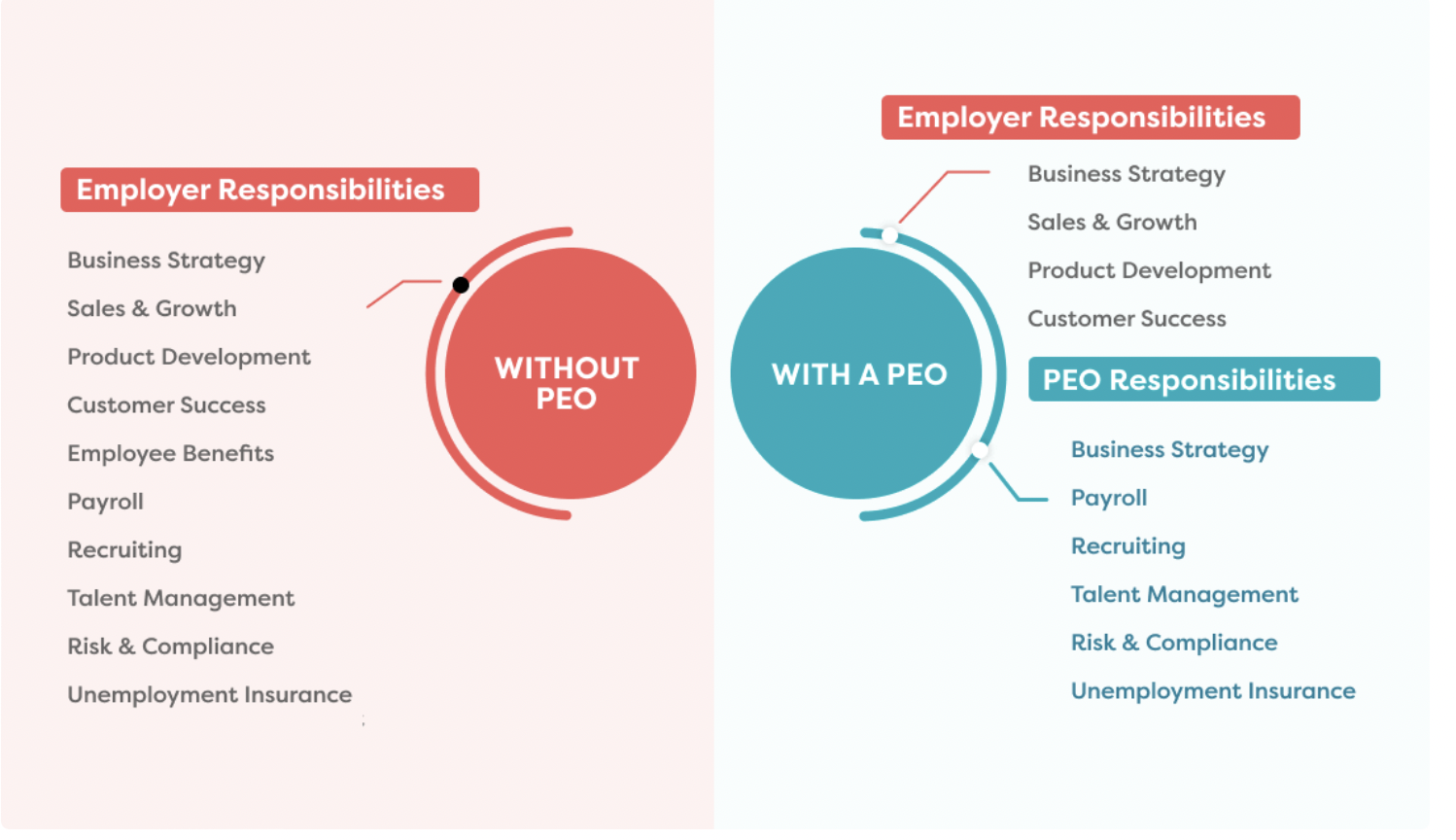

Managing payroll is a critical function that can be handled either by an in-house team or outsourced to a bookkeeper or PEO. It really depends on the specific needs and nature of the startup.

In the case of early stage startups, outsourcing payroll to a professional bookkeeper can save time and reduce the administrative burden on business owners and internal staff. As your startup scales, transitioning to an in-house payroll system can offer significant advantages. It provides greater control over the payroll process, ensuring immediate access to financial data and enabling quicker responses to employee inquiries.

A good option might also be a PEO. PEO is defined as a professional employer organization.They offer comprehensive HR solutions for small and mid-sized businesses, including payroll, benefits administration, HR support, tax management, and regulatory compliance assistance.

A PEO provides the flexibility to hire across various locations around the world without the need for you to register in each one. Additionally, a PEO can manage employee benefits, eliminating the need to hire an in-house benefits specialist. This arrangement often grants access to better rates for medical benefits due to the PEO's larger pool of clients. It is important to be selective in PEO vendors as we have experienced the headaches of constant billing issues especially if you are trying to capture cost by location. Please make sure to interview a couple vendors before you select.

Alternatively, you can have an in-house HR team which comes with its own set of benefits. In-house HR provides maximum control over HR processes and policies and you can shape your HR department to align precisely with your company’s culture and goals.

Based on our own experiences, we believe that businesses shouldn't have to choose between a Professional Employer Organization (PEO) and an in-house payroll team. Utilizing both can be a strategic advantage for companies at any stage of their growth.

When we were a part of a start up with an employee count of less than 25 and operating with a tight budget, we leveraged a PEO to provide our employees with quality medical benefits. In some U.S. states, larger groups (100+ employees) benefit from more favorable medical premium rates. By using a PEO, we were able to access these rates, ensuring our employees—our most valuable asset—receive top-quality care while keeping costs manageable for the company. Surprisingly, even after growing to a company of more than 2,000 employees and becoming publicly traded, we continued to use a PEO globally alongside our robust in-house payroll teams and systems. PEOs were invaluable in testing our go-to-market (GTM) expansion strategies worldwide. Often, leaders were eager to enter new markets but overlooked the costs and risks associated with hiring in unfamiliar territories. For instance, establishing an entity too early in countries with strict labor laws can mean being obligated to pay years of salary for an employee who may have only worked a few months

E : Equity

To attract and retain top talent, offering ownership shares in your startup is often essential. Top-tier talent aren’t going to leave high paying jobs for a lower salary and the desire to work at a “cool” startup. Depending on the employee's role and contributions, equity is typically offered in addition to a base salary. This isn’t limited to employees. You are going to most likely offer it to advisors, consultants, and strategic board members.

However, before deciding on your company's compensation structure, it's crucial to understand the key differences between various equity compensation forms, such as Stock Options , Restricted Stock Units (RSUs), and Performance Share Units (PSUs) each representing a form of ownership in the company and carrying different tax implications.

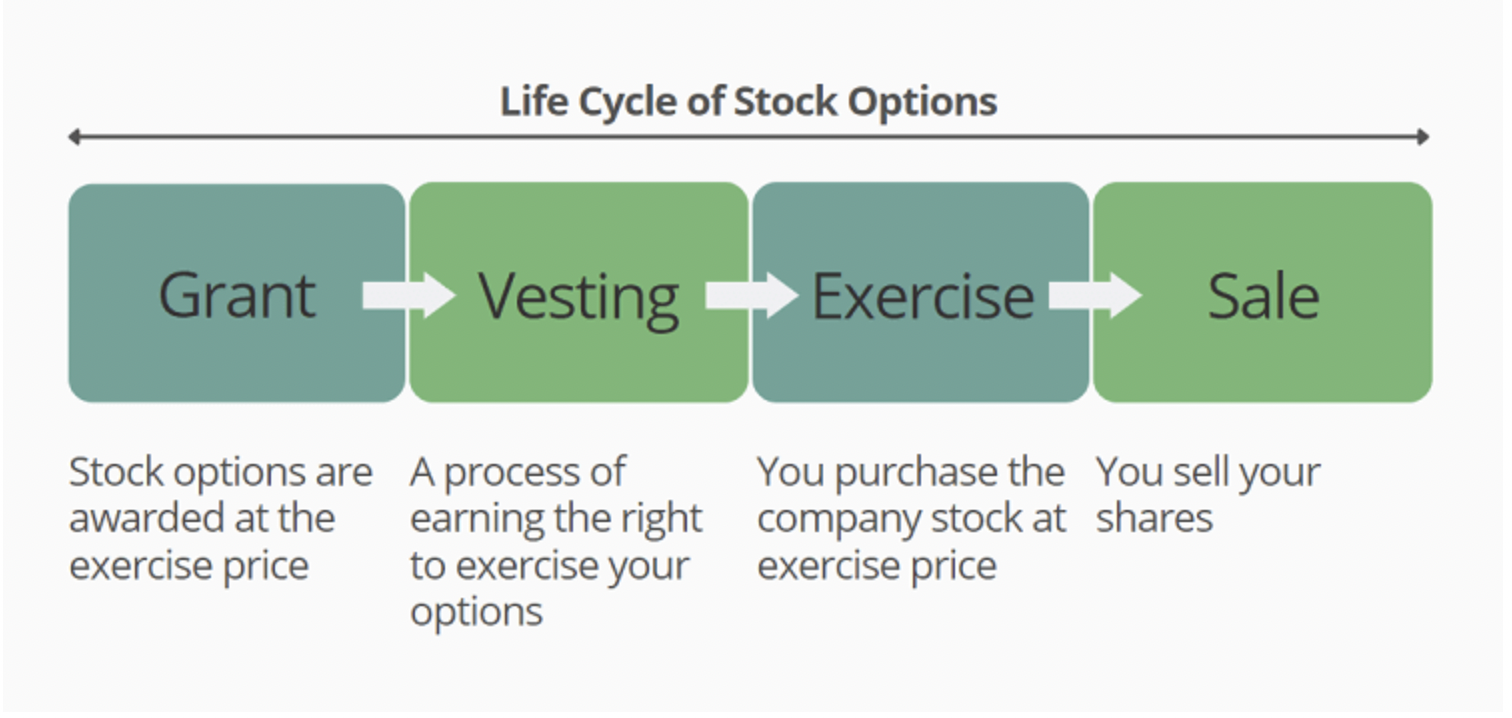

Stock optionsare a form of equity compensation that gives employees the right to purchase a specific number of company shares at a predetermined price, often referred to as the grant, strike, or exercise price. While stock options aren't actual shares of stock, they provide the opportunity to buy shares at the fixed price, potentially allowing employees to profit if the stock's value increases over time. The key benefit is that if the stock's market value rises, you can sell the shares for more than you paid, but you are never obligated to exercise the option—hence the name "options."

In our experience, this has been the most popular form of equity compensation for startups. You might want to use a legal advisor or companies like Carta to help you set up your Incentive Stock Options Plan. You'll need to establish vesting schedules for your incentives. The most common structure is a 4-year schedule with a one-year cliff and monthly vesting thereafter. The purpose of a 'cliff' is to prevent the distribution of stock to employees who leave within the first year and mainly applies to new hire grants. For existing employees receiving additional stock options, the cliff is usually waived, and they vest monthly starting from the grant date. However, in a competitive job market, some companies are choosing to forgo the cliff even for new hires and are shortening the vesting period to 3 years.

But what about RSUs?

A Restricted Stock Unit (RSU) is a commitment made by an organization to grant an employee shares at a future date (known as the vesting date), provided certain conditions are met. These conditions typically include remaining employed with the company for a specified period.The vesting of RSUs can also be contingent on specific events, such as an initial public offering (IPO) or the acquisition of the company by another entity.

But you need to be aware of the potential downsides of RSUs. Unlike Stock Options, once the RSUs vest, they are considered income, and a portion of the shares is withheld to cover income tax obligations. The remaining shares are then transferred to the employee.

As such, you would usually want to avoid granting RSUs with a vesting schedule until your company goes public and your stock is liquid. Otherwise you need to withhold income tax on vested shares even though the shares cannot be monetized. However we see RSUs where vesting is tied to an exit event being more and more popular. In this case, you don't expose your employees to income tax withholding unless there is an exit event like IPO or M&A and they can actually sell shares.

This brings us to PSUs.

Performance Share Units (PSUs) are awarded to employees based on the company's long-term performance, with the number of PSUs granted often tied to the company's achievement of key metrics over a specified period, typically three years. PSUs are typically reserved for upper management. The more the company exceeds its performance targets, the more PSUs are awarded to participants. Common metrics used to determine success in a PSU plan include earnings per share, return on capital, and total shareholder return. While it sounds great, there are drawbacks to PSUs. They can be costly for your company, depending on the specific terms of the plan. Additionally, there's a risk that employees might take reckless actions if they know they are close to receiving a substantial reward, even if those actions aren't in the company's long-term best interest.

R: Records/ Systems

Next up is having an accounting record system in place, below are some options to consider.

QuickBooks is highly popular for a company due to its user-friendly interface and features tailored for small businesses, making it ideal for managing day-to-day accounting tasks. However Quickbooks can be outgrown.

NetSuite offers a more comprehensive solution, integrating advanced accounting capabilities with CRM and e-commerce, which is perfect for scaling startups. We would recommend implementing Netsuite when you get close to starting generating revenue. Netsuite was able to grow with our companies north of $1B in revenue.

Bill.com simplifies accounts payable and receivable, streamlining bill management and payments.

Carta is essential for startups dealing with equity management, offering tools to manage cap tables, valuations, and equity plans.

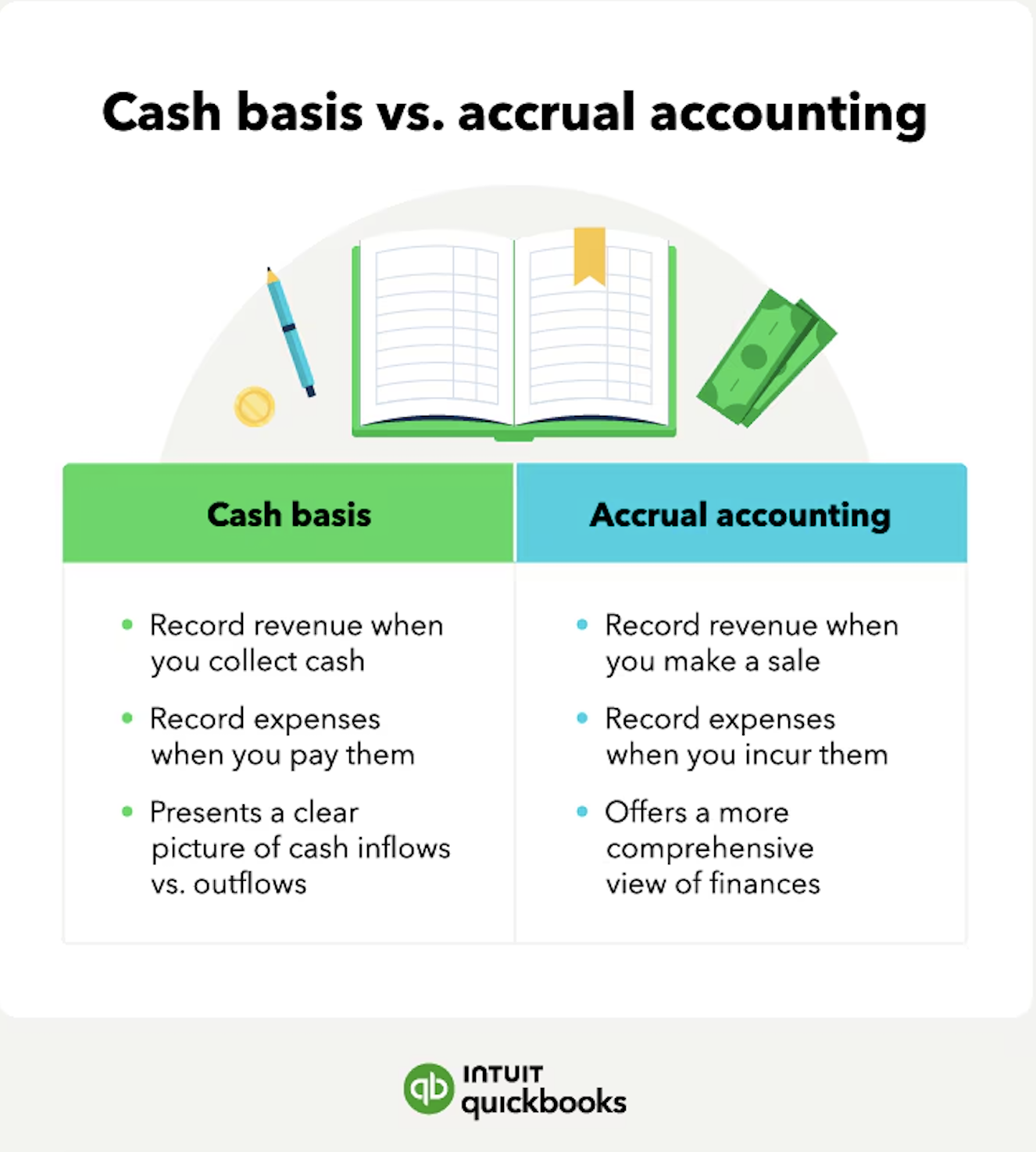

A : Accounting Methods (Cash vs Accrual)

As a founder, you’ll need to choose one of two possible accounting methods for your company:

- Cash Basis Accounting: Cash basis accounting is the simplest form of accounting, where income is recorded when it is actually received, and expenses are recorded when they are actually paid. This straightforward approach makes it easy to track cash flow however this approach is not GAAP compliant and might make it difficult to measure your performance against your peers.

- Accrual Basis Accounting: Accrual basis accounting records income when it’s earned and expenses when they are incurred, regardless of when the money is actually received or paid. Accrual Basis Accounting is what is required under US GAAP. This is more complex but provides a more accurate and long-term picture of the business.

Accrual based accounting doesn't always have to be a full US GAAP compliant set of books. In an early stage you probably don't need to do complex accounting for i.e. Stock Based Compensation, Research & Development capitalization or Tax Provisions. These you will need when you have to have audited financial statements which might be required in some situations i.e. to get a next round of financing or certain loans.

We recommend hiring an expert at that time to help you and your bookkeeper convert your records to be fully compliant with US GAAP.

T: Taxes

Being a startup does not exempt you from tax obligations. You may be subject to the following types of taxes:

Payroll tax- is a tax paid on the wages and salaries of employees to finance social insurance programs like Social Security and Medicare

State and local taxes- is a tax assessed by state and local governments for conducting business in their jurisdictions

Sales and use tax - is a tax imposed by state and local governments on the sale or use of goods and certain services

Gross receipts taxes- is a tax on the gross receipts of a business for all taxable business activities attributable to certain cities and states.

Personal Property tax- is a tax levied on movable assets owned by individuals or businesses, such as vehicles, laptops, and equipment.

It is important to discuss these types of taxes and plan with your outsourced bookkeeper to stay in compliance.

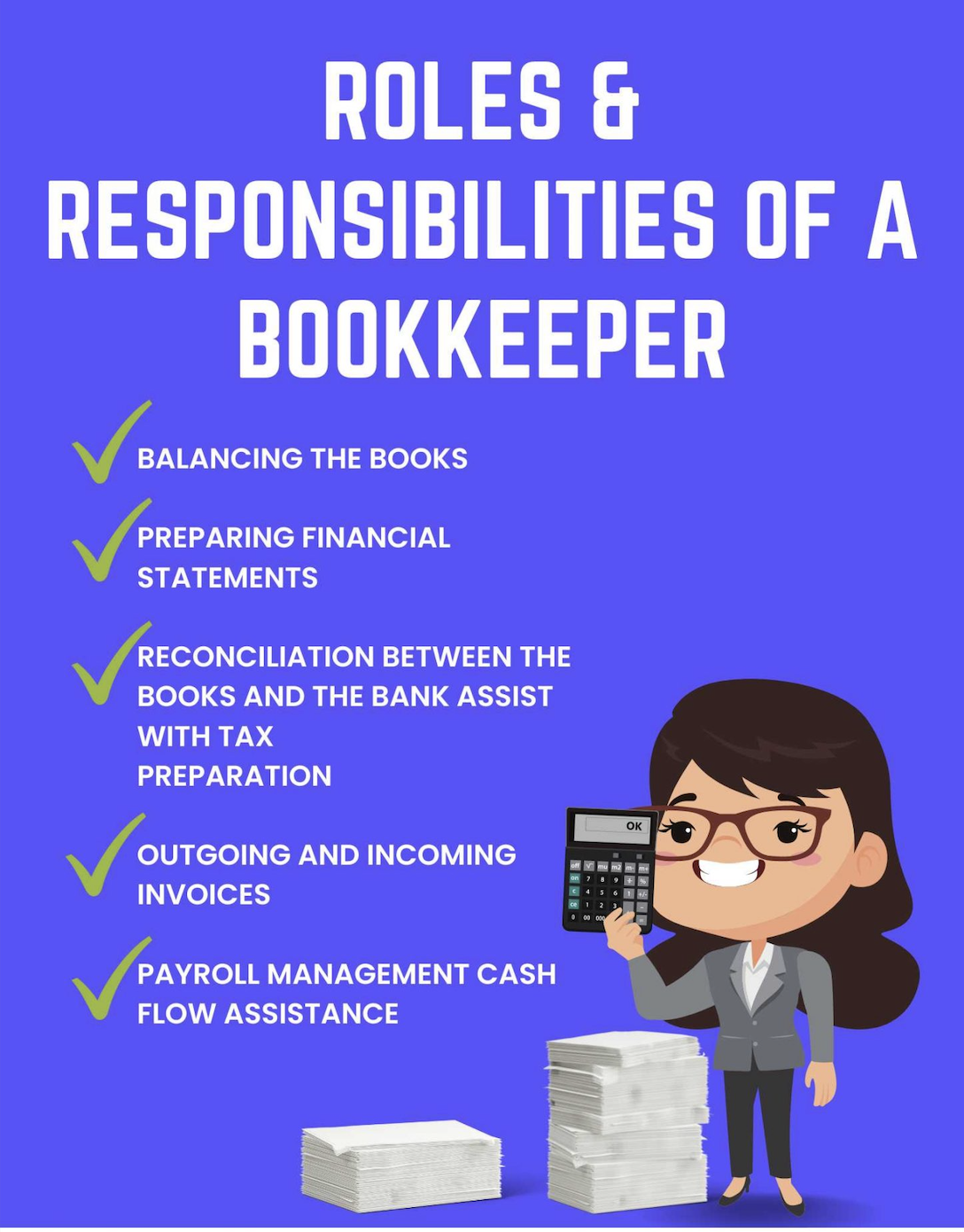

O: Outsourced Bookkeeper

Choosing the right bookkeeper matters.

It can significantly impact your future success and alleviate stress. Opting for the cheapest option doesn't always translate to better service (and you don’t want to learn this the hard way). Please note when starting out your business you can expect your bookkeeping should only take a couple hours a month and should not be someone’s full time job. It is also reasonable if you are an early stage startup to expect your bookkeeper to close your monthly books in a few days. We often hear stories when companies don't get their books closed in weeks following the end of the month. It is crucial you set up expectations with your bookkeeper before you commit to them. Having financial information timely is essential to make decisions and run your business, otherwise this information becomes obsolete by the time you get it.

Keep in mind that a skilled and experienced bookkeeper can provide invaluable insights, ensure accurate financial records, and help you navigate complex accounting tasks. By cutting corners, you leave yourself open to risk and mistakes that can prove costly.

R : Risk Management

Fraud is widespread, and startups are especially susceptible to it.

A 2022 report by the Defense Logistics Agency estimates that the average organization loses 5% of its annual revenue to fraud each year, causing a median loss of $117,000 before detection. We've personally encountered numerous phishing attempts and email scams that can jeopardize financial security.These email scams included a bad actor inserting himself in the middle of a company and vendor email thread. The bad actor proceeded to request legit vendor payments to be sent to a fictitious bank account.

Please also note that fraud scams are not just external and can come from inside your organization as well. Sometimes even the “superstars” can be the ones to commit the fraud. Having experienced first hand a highly respected employee committing fraud was very eye opening. This can happen to any company at any stage. We've seen this occur in both well-established public companies with strong internal controls and in early-stage startups. We provide additional insight here to protect you and your business.

Conclusion

Accounting can be complex and overwhelming, especially for first time founders.

By following our OPERATOR model, we hope to simplify financial management and empower you to keep a better track of your startup’s finances. Please make sure to keep in mind that you don’t need to have everything done on day 1 depending on your firm’s structure and complexities. The most important thing to keep in mind is making sure you have a rough idea of what are the major milestones you need to be aware of. If you are not sure of what those major milestones should be, talk to someone who can guide you. This is an ongoing process and you should continue to assess and adapt according to the progress of your business.

With a better understanding of your financial health and the tax requirements, you can make informed decisions and allocate resources more effectively. We hope this frees up valuable time and energy to focus on the innovation and strategic growth that drives all startups.

Find your ideal investors now 🚀

Browse 10,000+ investors, share your pitch deck, and manage replies - all for free.

Get Started

About the author

KB&A Accounting was founded by three professionals Kasia, Barb & Angel who honed their skills at some of the world's most reputable companies. Driven by a passion for problem-solving and helping businesses navigate operational challenges, they launched KBA to provide expert support to founders, CFOs, and business owners. Since its inception, the firm has helped clients build solid financial foundations, optimize processes, and prepare for key milestones like audits and securing funding. For all your accounting needs, feel free to reach out to us at KBA Accounting or email us at [email protected].

This article is for general informational purposes only and should not be construed as tax, legal, or accounting advice. You should consult with a qualified professional before making any decisions based on the information provided

![12 Best Startup Financial Model Templates [Free & Paid]](https://d1pnnwteuly8z3.cloudfront.net/images/177302d9-3657-45b7-ac9d-acf801d83a74/1b029edf-43cf-4bd9-9e37-203f66bf426f.png)