Venture capital is all the rage these days. Whether you are a fresh out of college and want a job at a hot firm or a founder looking to raise capital for the first time, it seems that everyone wants to be in VC.

But when did all this begin? How far does venture capital go back? Did the ancient Egyptians pitch the pharaohs on a pyramid that would be disruptive and an improvement on the ziggurat? Was Christopher Columbus' discussion with Queen Isabella regarding the financing of his journey of exploration truly a startup pitch? Or is this something that was born recently in terms of the historical scale?

In this article, we are going to explore the history of venture capital and how it has evolved over the years. Now before you bemoan how history is a collection of dates, places, and people that no longer matter, you need to realize how paramount VC history actually is.

Why?

Because current and future VCs can benefit from our predecessors in the industry. VC is still a relatively young industry and by standing on the shoulders of giants, you can give yourself a major advantage.

Let’s get after it.

Table of Contents

1800s: A whale of a VC tale

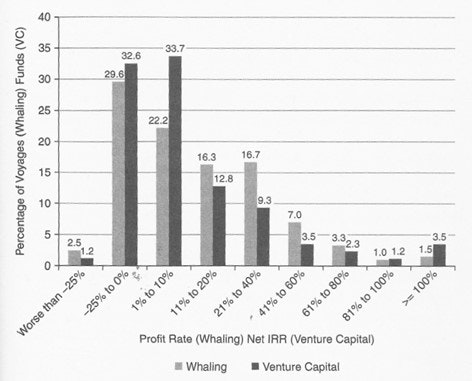

If you want to know the origins of modern venture capital, then Harvard professor Tom Nicholas has you covered. In his book, VC: An American History, Nicholas discusses the history of VC in the United States. In an interesting comparison, Nicholas focuses on the whaling industry.

“Nineteenth century whaling can be compared to modern venture capital… Whaling was the archetypical skewed-distribution business, sustained by highly lucrative but low-probability payoff events… The long-tailed distribution of profits held the same allure for funders of whaling voyages as it does for a venture capital industry reliant on extreme returns from a very small subset of investments. Although other industries across history, such as gold exploration and oil wildcatting, have been characterized by long-tail outcomes, no industry gets quite as close as whaling does to matching the organization and distribution of returns associated with the VC sector.”

Like the startups of today, whaling expeditions had high costs and extraordinary risks (except being lost at sea is a rare danger for the founders of today). Yet they also had high returns if they were successful. In the following chart, Nicholas compares returns of the top 29 whaling ventures to the returns of the top 29 venture capital funds, nearly two centuries later. Thank you to American Business History for the chart.

Nicholas doesn’t just stop with whaling expeditions. The industrial revolution (specifically the development of the spinning Jenny) and the laying of the railroads that connected cities across the continental United States, were both financed by wealthy investors (with railroads also relying on government investment) that are similar to the VC deals of today.

1880s-1890s: Let there be light

In the late 1880s, the war was on between Thomas Edison and Nikola Tesla. Edison was a proponent of direct current while Tesla supported alternating current. Much like the argument over a century later between your friends on which was cooler, Facebook or Myspace, there could only be one victor.

R.I.P Myspace, where Tom always had your back.

Finance titan J.P. Morgan backed Edison, becoming the first true technology investor (and beta user, as Edison installed lightbulbs throughout Morgan’s estate). Tesla was backed by entrepreneur George Westinghouse. Ultimately Edison’s direct current won the day, especially for J.P. Morgan, whose company that backed Edison later became General Electric.

General Electric went on to become one of the original dozen companies to be listed on the Dow Jones. GE now employs over 200,000 employees and the term “lit” can be traced back to their investments in Edison’s technology.

1946: Modern VC

The beginning of modern venture capital dates specifically to 1946.

Why 1946?

Because that is when the first true venture capital firm was incorporated. American Research and Development Corporation (or ARDC as the cool kids call it) was formed by a team that could rival the Avengers.

And just who was this team?

- Massachusetts Investors Trust chairman Merrill Griswold.

- Karl Compton, the president of MIT.

- Ralph Flanders, the president of the Federal Reserve Bank of Boston.

- General Georges F. Doriot, a Harvard Business School professor whose referred to as the father of venture capital.

Or by his street name, “the OG of VC.”

So what did ARDC do that was so different and radical?

Simple.

They raised their capital from investment trusts, mutual funds, insurance companies, and universities.

Why was this such a big deal?

Because before the formation of ARDC, there were only a few sources of capital for private companies. In those old timey days in the United States, you had to seek an audience with an established family. The Whitneys, Rockefellers, or Vanderbilts were the main source of capital (although we can’t confirm it, we can assume it was much harder to get a pitch meeting before the advent of email, PowerPoint, and Docsend).

As venture was more about who you knew and not an industry, the great companies of the past had to rely on bank lending, government funding, mergers, and the issuance of stocks and bonds to raise capital. This changed with ARDC.

ARDC was a public company that bypassed these families. They showed that there was interest from institutional investors in private companies seeking capital. Like firms today, ARDC invested in technology companies. ARDC’s most notable success story came from their $70,000 investment in DEC, the Digital Equipment Company in 1957. Over the next fourteen years, the value of DEC increased to $355 million, showcasing that a VC firm could make a major return and demonstrating the first example of the power law.

There was another reason that ARDC was so paramount in the history of VC. Many of its employees would later launch their own firms.

1950s-1960s: Welcome to the Rock

Few have had such an impact on the VC industry as Arthur Rock. As an investment banker in the 1950s at Hayden, Stone & Company, Arthur Rock was at the right place at the right time. A letter from Eugene Kleiner and his peers, who wanted jobs together at a new company (their current employer, Shockley Semiconductor Laboratory was a toxic work environment to say the least, with founder Dr. Shockley being prone to paranoid outbursts), arrived on his desk. Arthur Rock had a a better idea.

Why not form a new company rather than find the men employment?

This group, known as the Traitorous Eight, formed Fairchild Semiconductor.

Why was this so pivotal for the world of VC? Arthur Rock said it himself:

“And so we divided up the company. They each got 10 percent, which amounted to 80 percent, and Hayden Stone got 20. And that’s where the famous 80-20 began with. For all you venture capitalists, if there are any in the room, you can thank me for your 20 percent.”

That would be enough if that was Arthur Rock’s only contribution to VC, but he was just beginning. Constant trips from New York to Palo Alto (then nothing more than a backwater suburb) led Rock to establish what would become a bedrock of VC and Silicon Valley.

“When I started coming out with Fairchild Semiconductor, I realized that there were a lot of small companies around this area that were looking for capital, and the capital was all in the East. And that I thought that maybe I could bring some of the Eastern capital out to the Wild West. I saw that the people were much more entrepreneurial here and were willing to take on chances that people on the East Coast were not.”

In 1961, Rock moved to California and setup Davis and Rock, the Bay Area’s first venture capital firm. Raising $5 million from his own personal network, Rock only used $3 million of the funds raised to invest in 15 companies, generating $100 million in returns. His basis for investing was based around the founders, setting the stage for what modern VC uses for talent spotting and founder fit.

“Well, it's all about the people... Good ideas and good products are a dime a dozen….good people are rare.”

Arthur Rock went on to continued success, helping find investors for some new startup called Intel (where he was an active member of the board and his share was 10% of the company), investing early in Apple at the time that Steve Jobs still was the smelly kid, and became the first venture capitalist to grace the cover of Time Magazine, no big deal.

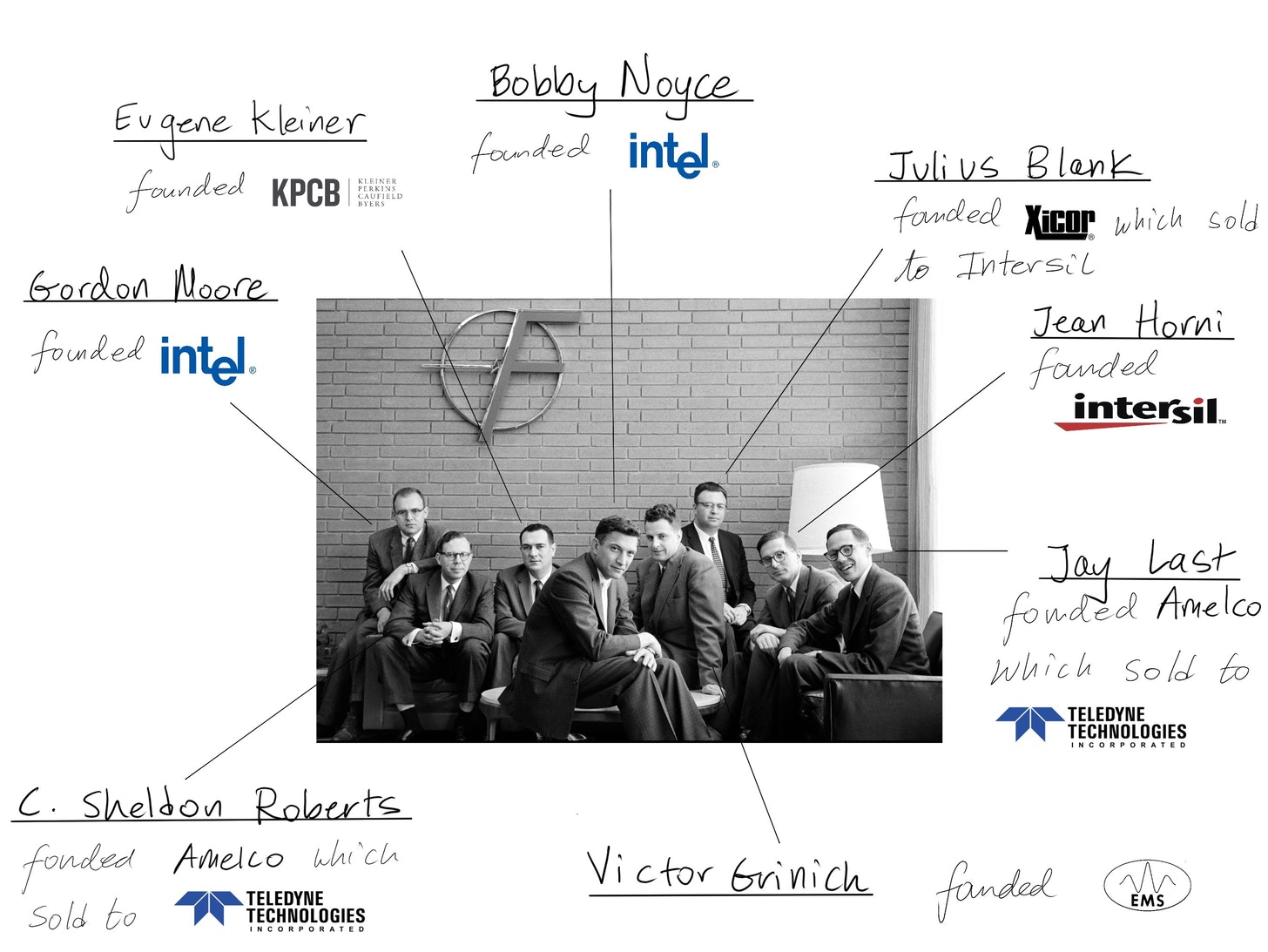

And what of the Traitorous Eight who Arthur Rock supported and convinced to begin Fairchild Semiconductor? They played a major role in developing that backwater I mentioned into the Silicon Valley we know today. They went on to found their own companies. A big thank you to Mario at The Generalist for the following infographic:

Mario also goes further :

“As of 2014, an estimated 92 companies trace their roots back to Fairchild Semiconductor founders and employees (some suggest the number is closer to 400), with $2 trillion in value created. That includes Apple, Advanced Micro Devices, and Applied Materials, as well as venture firms like KPCB and Sequoia.”

All because a group of fed-up employees could smell what the Rock was cooking.

“It is entirely possible that there would be no silicon in Silicon Valley if Fairchild Semiconductor had not been established. The Fairchild Eight would probably have dispersed and the only other company working with silicon was Texas Instruments.”-Arthur Rock

1960s-1980s: VC becomes an asset class

In the 1960s, VC was still a cottage industry. This didn’t stop eager investors from establishing their own firms, many of which are still operating today. Here are a few of them.

- Asset Management Company

- Mayfield

- Morgenthaler Ventures

- Sutter Hill Ventures

- Fidelity Ventures

- Greylock

But it was the 1970s that saw the founding of the largest firms of today.

- Matrix Partners.

- Oak Investment Partners.

- Menlo Ventures.

- New Enterprise Associates.

- Sequoia Capital.

- Kleiner Perkins Caufield & Byers.

- Bessemer Venture Partners (although Bessemer Securities previously existed as a family office).

Interestingly, Sequoia was founded by Don Valentine who was a salesman at Fairchild Semiconductor. And Eugene Kleiner of Kleiner Perkins Caufield & Byers was one of the eight co-founders of Fairchild Semiconductor (thank you for the help uncle Rock).

Speaking of Kleiner Perkins Caufield & Byers, Tom Perkins popularized a model of investment that was beyond a simple influx of cash. In addition to investing into young fledgling startups, Perkins also sought to provide advice and counsel to further their growth. This began the value-added investor style of today where VCs are active managers rather than silent partners.

“If there is no risk, you have already missed the boat.”-Tom Perkins.

In 1973, the National Venture Capital Association (NVCA) was formed in the United States so that VC could have a voice in Washington. They continue to advocate today for VC firms, their portfolio companies, and the entrepreneurship ecosystem. It was also during this period that VC firms also officially began the Limited Partnership model. This is the corporate structure that is now ubiquitous in venture capital.

More importantly, changes to the Employee Retirement Income Security Act’s (ERISA) “prudent man rule” in 1979 was a major boost to VC. In simple terms, pension funds were now able to allocate up to 10% of their capital to VC funds. Before this change, VC was seen as too risky. Pension funds continue to be a major source of long-term capital to venture capitalist firms.

It should be noted that since 1974, 42% of all companies to go public have been venture-backed.

By the 1980s, it was a great time to be in VC. Risky companies that were backed by VCs had their exits, providing major returns and becoming household names in the process. You may have heard of a few. Apple, FedEX, Microsoft, and Genentech.

But it wasn’t until the 1990s and the rise of personal computing that VC really took off.

1990s-2000s: Something called the Internet

In the early to mid 1990s, personal computer usage boomed. Once regulated to the office and the classroom, computers were now increasingly found in more and more homes. More importantly, these homes were becoming connected to the world wide web, or the internet as the cool kids called it.

This was the decade that brought us many companies which are now household names. Venture backed companies in this decade include:

- America Online

- E*Trade

- Paypal

- eBay

- Netscape

- Amazon

- Yahoo

- Netflix

- Salesforce

It should also be stated that corporate venture capital (CVC) units flourished in this era. A CVC is an investment of corporate funds directly into startups via their own venture capital arms.

In 2000 alone, more than 20 new CVC groups made their first investment, according to CB Insights data. Close to 100 CVCs made their first investments in the years between 1995 and 2001. The total investment amount from deals involving CVCs grew to approximately $17B in 2000. That was 25% of total funding to VC-backed companies in that year.

Everyone wanted in. It was a glorious time to be a tech founder and a venture capitalist. Money flowed as more and more companies sought to take advantage of the expanding internet and its endless possibilities.

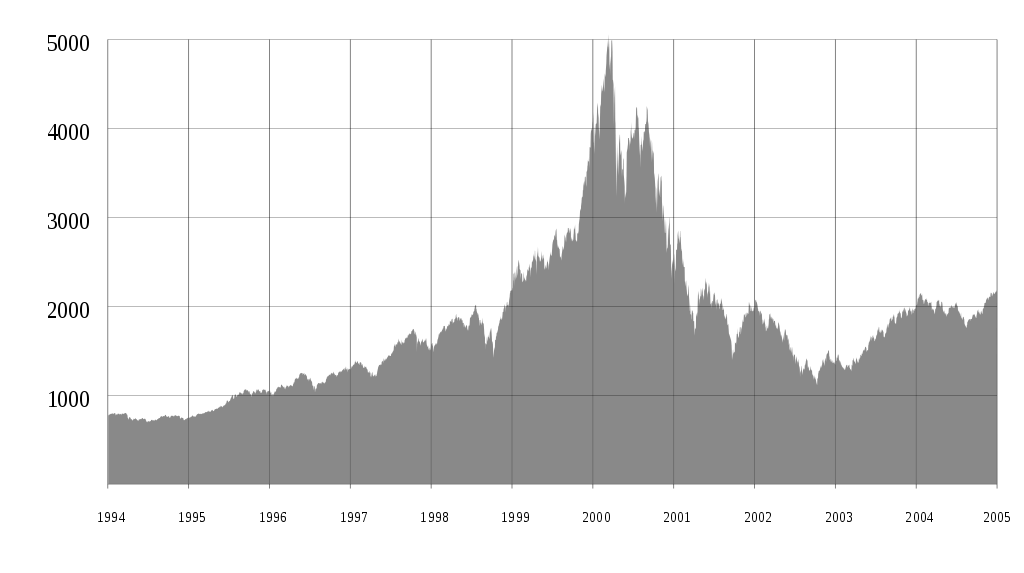

But it wasn’t all champagne and 56k modems. This period saw the rise and fall of many companies, all riding high on the possibilities that the internet and the proliferation of technology could provide. That was until the dot-com bubble burst and took many venture dollars with it. Here is a chart of the NASDAQ Composite index which spiked and then fell sharply with the dot-com crash.

Venture backed failures of this time include:

- Boo.com, an online clothing store which burned through $135 million in two years.

- Webvan, an online grocery store, which had a $1.2 billion valuation but within two years, was liquidated.

- Pets.com, an online pet supply store in which Amazon owed 50%, had a $82.5 million IPO yet closed down a mere nine months later.

And those CVCs previously mentioned ? They took major hits. $9.5 billion of venture related losses were written down in the second quarter of 2001.

- Microsoft wrote off more than $5.7B in 2001.

- Wells Fargo wrote down $1.2B.

- Intel wrote down $632M.

Microsoft, AT&T, and News Corp, as well as many other companies disbanded their CVC arms. Others liquidated their holdings through fire sales. Starbucks decided to no longer invest in startups (instead focusing on creating new drinks, but that is an article for another time) along with Amazon, which learned the hard way through its investment in Pet.com.

2000s-2010s: After the dot-com bust, enter the accelerator

Despite heavy losses and the notion that the party was over, the world of VC post dot-com crash saw a shift. Although tech company valuations were destroyed and many investors had lost their capital, the promise of new technology and innovation continued to draw VC investment. VC firms now focused on certain sectors, industries, or stages. The 2000s to the mid-2010s saw an era dominated by software, services, GPS, mobile, and of course, a new industry that would be called social media and take the world by storm.

This is what a Bootstrapped Facebook looked like when I joined and it was only open to the kids at the cool schools.

This was also an era that saw the birth of accelerators. In 2005, Paul Graham launched Y Combinator. Seedcamp launched in the UK in 2007. This was followed by a slew of accelerators including Techstars, Seedstart, 500 Startups, and others.

But what is an accelerator? The Harvard Business Review defines it in detail as:

Startup accelerators support early-stage, growth-driven companies through education, mentorship, and financing. Startups enter accelerators for a fixed-period of time, and as part of a cohort of companies. The accelerator experience is a process of intense, rapid, and immersive education aimed at accelerating the life cycle of young innovative companies, compressing years’ worth of learning-by-doing into just a few months.

Why did this play a role in VC and how did the firm benefit?

- Improves the deal flow pipeline. Accelerators are notoriously difficult for founders to get into (the average acceptance rate is 1.5% compared to Harvard’s acceptance rate, which is 5.9%). This creates higher quality investment opportunities as only top tier teams are admitted.

- Ability to network with other investors and a wide variety of founders.

- First access to new technology and ability to map trends in startups.

Notable companies to have gone through an accelerator program include:

- Airbnb.

- Dropbox.

- Stripe.

- Reddit.

- Twitch.

- Coinbase.

- Weebly.

- Udemy.

- Credit Karma.

This period also saw the beginnings of many offerings that are now commonplace in the startup and venture ecosystems of today.

- Investment marketplaces (AngelList, Seed Summit).

- Startup weekends.

- Pitch competitions.

- Startup schools (Founder’s Institute for example).

- Startup meetups.

- Hackdays.

- Venture incubators.

VCs also expanded on the value they brought to the entrepreneurs in their portfolio companies. Active management now included additional services such as marketing, recruiting talent, and business development.

2010 - present: Micro-VC

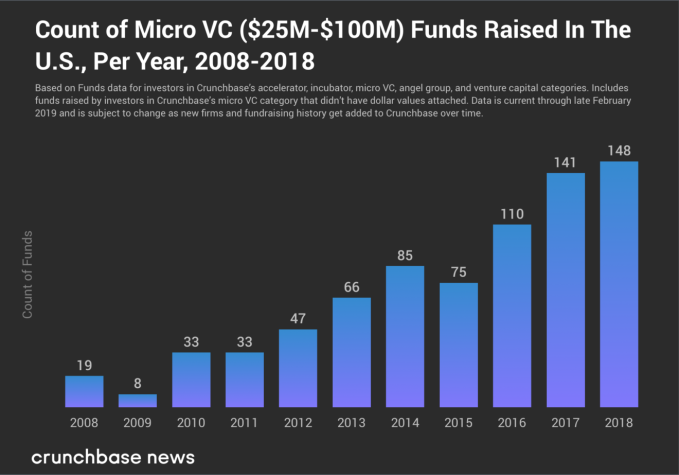

The 2010s saw the emergence of a new class of VC, the micro VC. As the cost of starting a company had fallen, opportunities were everywhere. Yet many VCs still refused to take a chance on such early stage companies. Thus, the micro VC was born to fill the gap. Micro VC firms are small firms whose fund size is between $25-$100 million. They invest small amounts of capital in a large pool of companies that are at the pre-seed and seed stage. This is a high risk and high reward strategy.

The majority of micro VC funds were started by experienced startup founders and former VC experts who are already connected into their respective startup ecosystems. This allows them to provide assistance, guidance, business solutions, and attract other investors to the founders in their portfolio companies. Thank you to TechCrunch for the chart.

Examples of micro VC funds include Arcus, Baseline Ventures, and Freestyle Capital. For a complete list of micro VC funds, you can visit EQVISTA.

Micro VC, along with CVC, hedge funds, mutual funds, and private equity funds, began to play a more important role for startups, especially at the early stages. The number of angel and seed deals completed reached a record peak in 2015.

This period also saw a new term enter the VC vernacular, the unicorn.

2013 - present: The unicorn era

With sky high valuations, the world of VC needed a new term to define a startup with a valuation of over $1 billion. Venture capitalist Aileen Lee answered the call, defining these startups as unicorns in 2013. Even though unicorns are fictional while these companies are real, Lee liked the term because “it means something extremely rare, and magical”

And just how rare are these unicorns? As of March 2022, the global number is now over 1,000 according to Statista.

VCs wanted in. Unicorn valuations mean major returns. This period was dominated by an influx of cash into promising startups who could become a successful unicorn and provide a major return to the VC.

But just because the valuation was high didn’t mean the company would be successful. Startups, despite being classified as a unicorn, are still inherently risky.

“The tech news may make it seem like there’s a winner being born every minute — but the reality is, the odds are somewhere between catching a foul ball at an MLB game and being struck by lightning in one’s lifetime. Or, more than 100x harder than getting into Stanford.”-Aileen Lee

Unicorns that failed included:

- Evernote

- Zynga

- Powa Technologies

- Quibi

- Theranos

Despite these failures, VCs continue to hope (and probably pray) that their portfolio companies can reach this valuation and have a successful exit.

2022 and beyond: VC today

Despite some slowdown, VC remains strong. Here are some 2021 statistics from the NVCA Yearbook :

- The U.S. accounted for 49% of $683 billion invested globally and 40% of just over 40,000 VC deals.

- 296 VC-backed public listings generated $681.5 billion in exit value in 2021, including 181 VC-backed IPOs that represented $512 billion. These 181 IPOs collectively had a post-money valuation of $614 billion, stemming from just $60.8 billion in VC funding invested prior to IPO. VC-backed IPOs accounted for nearly 20% of total U.S. IPO count last year.

- VC AUM (assets under management) reached $995 billion at the end of 2021, including $222 billion in dry powder. These assets were managed by 2,889 firms and 5,338 funds.

- The median size of VC funds in the traditional venture hubs of California, Massachusetts, and New York is $60M. Outside those states, the median is $29M.

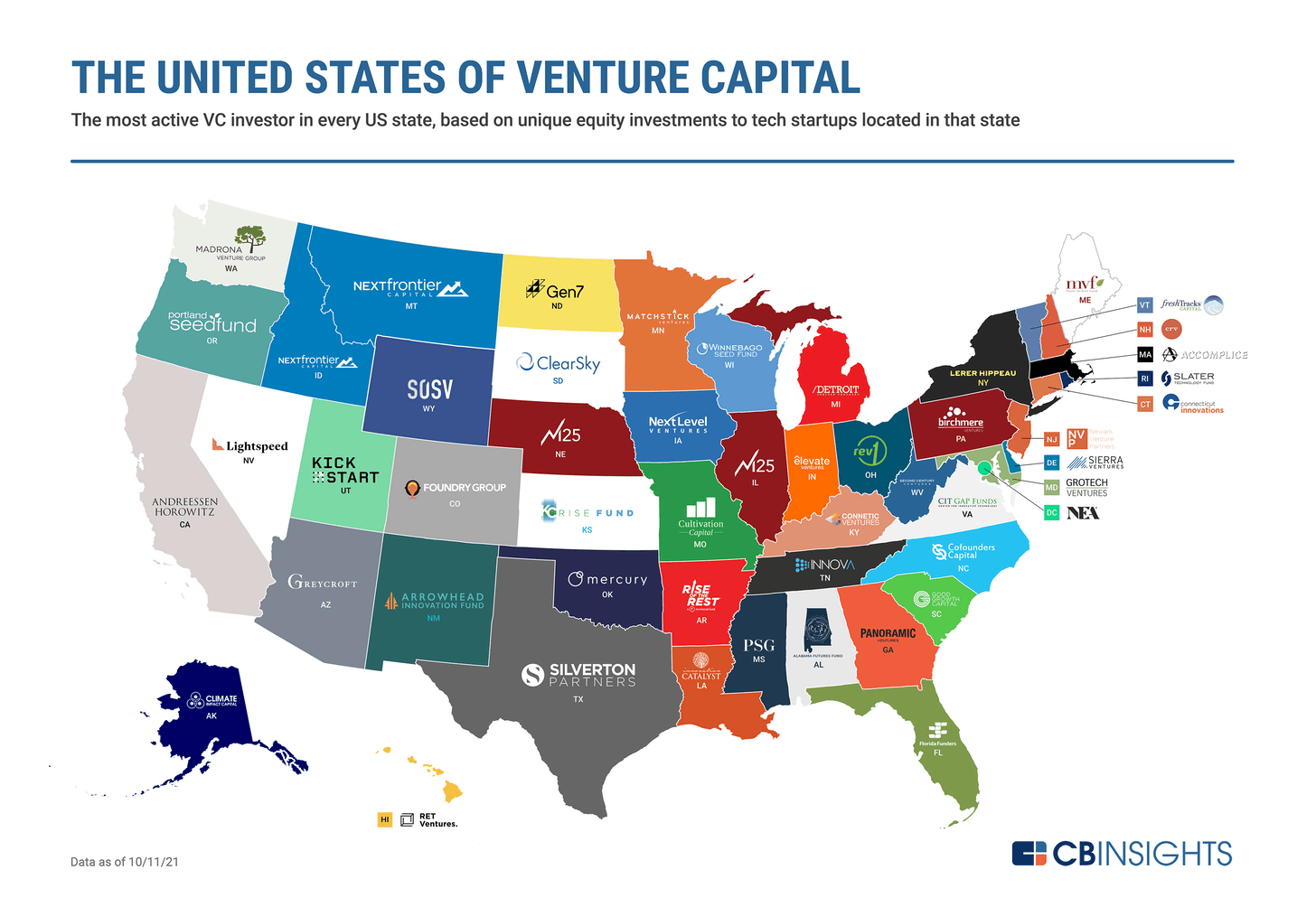

Furthermore, the following chart breaks down the most active VC investor in every state (thank you to CBInsights for the chart).

It also is worth noting that some of the largest and most successful companies were founded in a down market, being backed by bold investors with an eye on the future.

Keeping it all in check

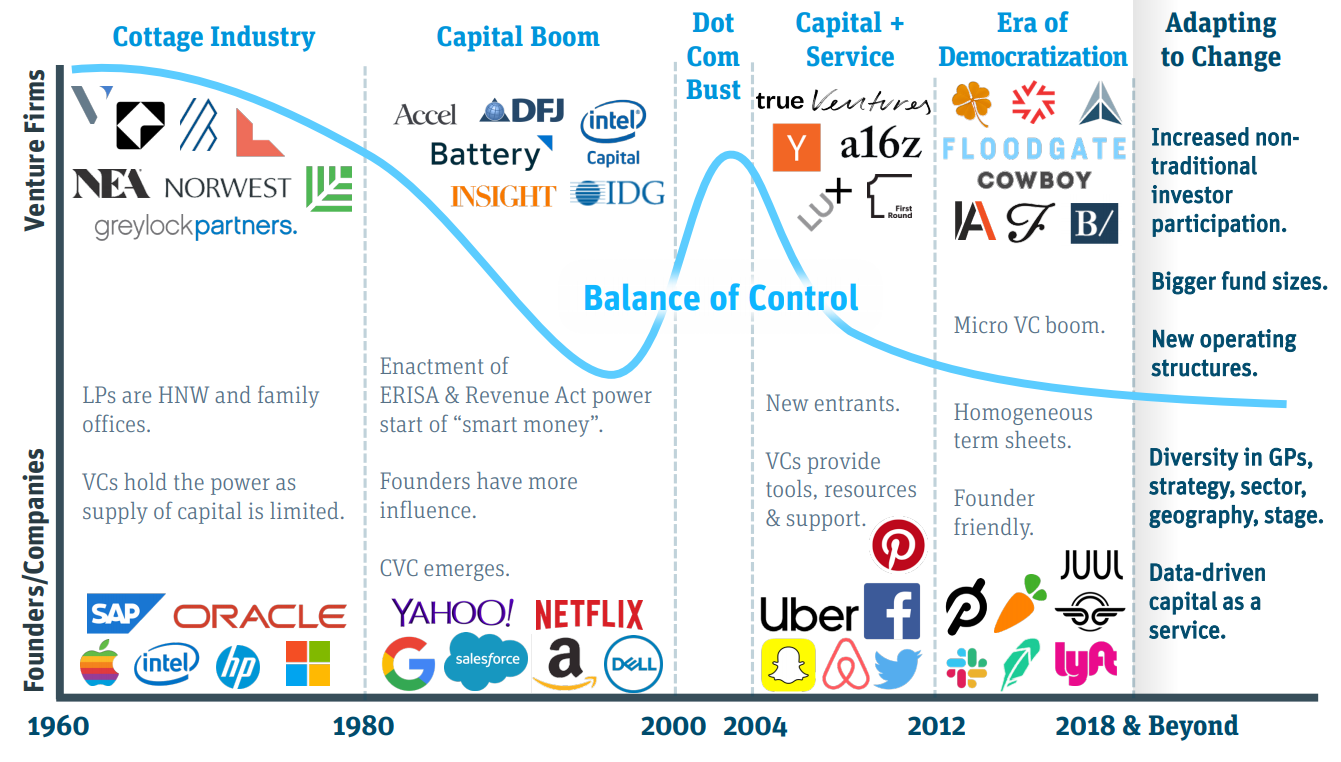

Wow, that was a lot of information. Here are two infographics to help you understand the history of venture capital. The first is courtesy of Venture Forward.

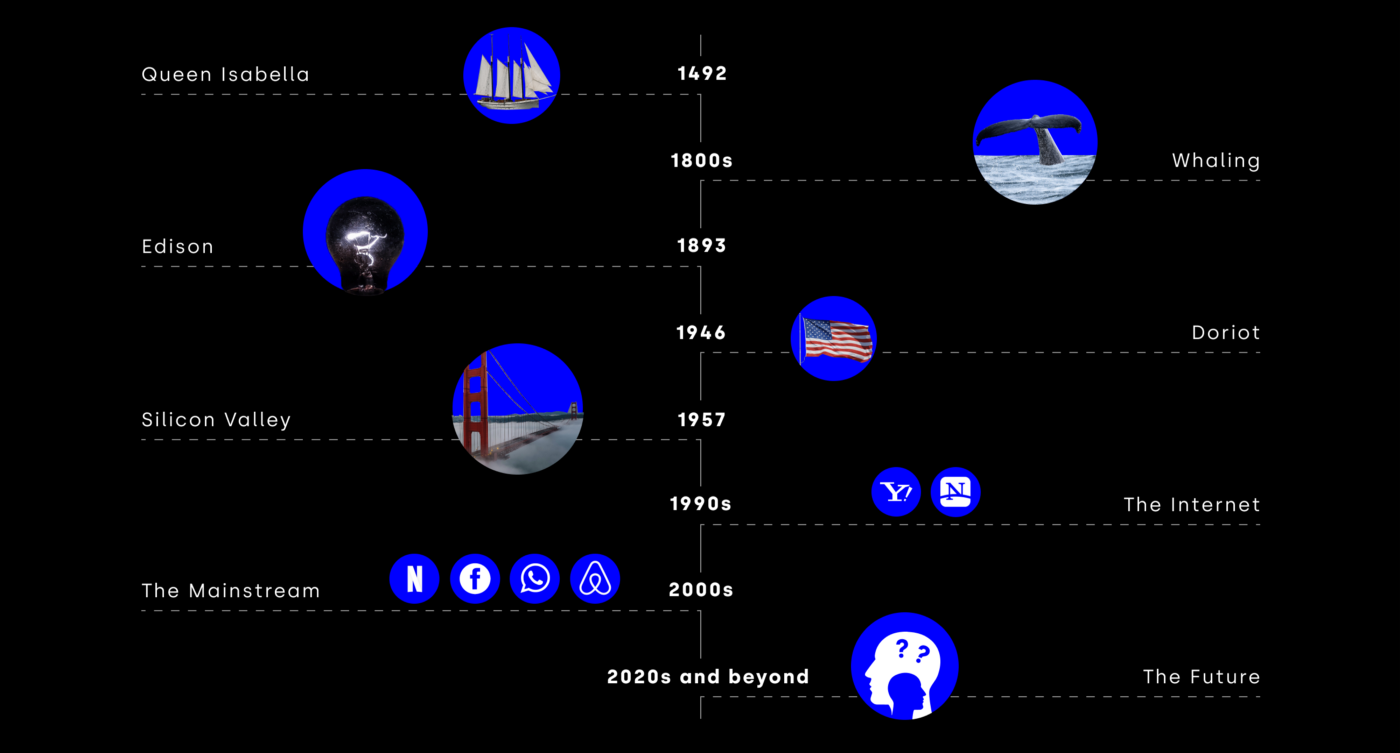

The next is a more simple but just as important timeline. A big thank you to Andrew Powell for this.

Conclusion

The history of venture capital is both exciting and interesting. By understanding that an entire modern industry was created by a few key individuals, it is hoped that you realize just how important your own role can be. The future is shaped by those who understand the past. By knowing the history of VC and the role it played in launching some of the largest companies in history, you will have an advantage to make your own mark.

Find your ideal investors now 🚀

Browse 10,000+ investors, share your pitch deck, and manage replies - all for free.

Get Started