Markets matter. A lot.

Founders tend to obsess over product, team, and distribution. And fair enough, that's the daily grind after all.

But before you jump in, get your market sizing right.

You're about to spend the next ten years building this company. The market you choose will shape what's possible. Before you write a single line of code or hire your first employee, make sure you're building in a market worth pursuing.

Table of Contents

1. Why Market Size Matters More Than Most Founders Think

Markets matter more than founders (yes, really)

There's an old debate in venture capital: do you bet on the horse or the jockey? The horse is the market. The jockey is the founder.

Marc Andreessen, arguably the most influential VC of the past two decades, came down firmly on one side. He said: "Market is the most important factor in a startup's success or failure." And separately: "The number one company killer is lack of market."

That's a strong take. But it's not wrong.

A great founder in a small market will still hit a ceiling. A mediocre team in a massive, fast-growing market can still build something meaningful. The market is the game you're playing. Choose it carefully.

VCs want a market size above $1B

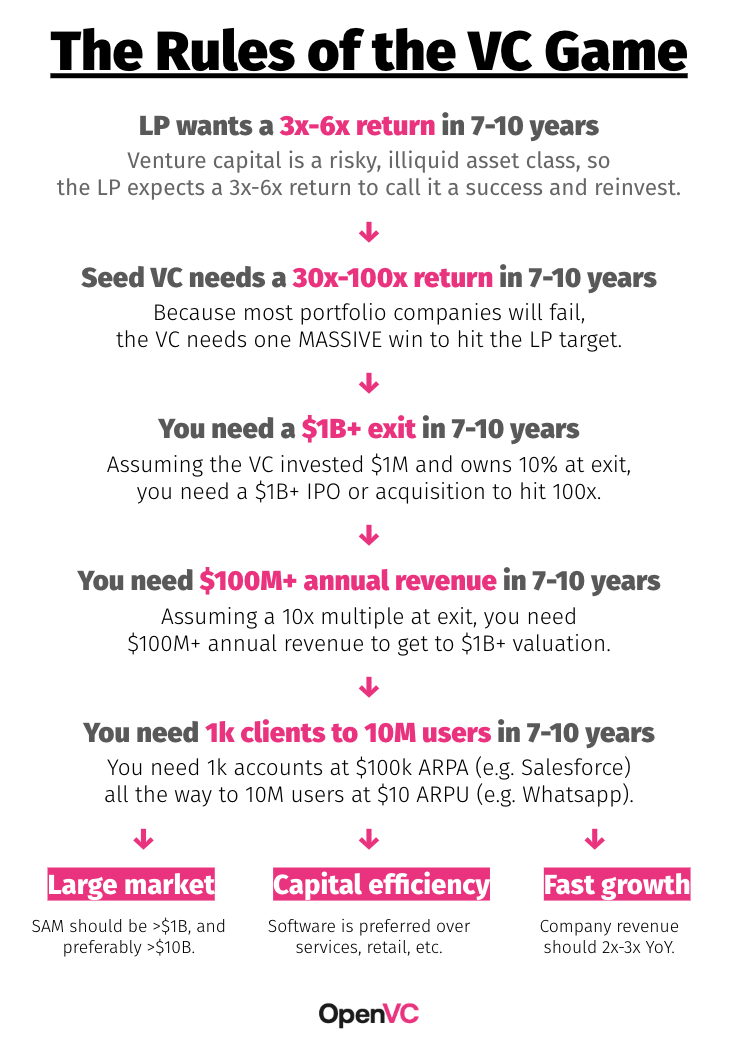

You've heard this before. But have you ever traced where it comes from? It's a backwards calculation, and it's worth understanding.

Start with the LP (the investor who put money into the VC fund). They typically want a 3x return over seven to ten years. The S&P 500 returns around 2.5x over a similar period, so given the illiquidity and risk of venture, 3x is the floor.

To deliver that 3x, a seed round VC needs roughly a 100x return on at least one portfolio company. Here's why: out of ten bets, five will return zero, four will return between 1x and 5x (barely covering losses), and the tenth has to return the whole fund. That's 100x.

To get to 100x: a $1M seed investment at 20% ownership dilutes to roughly 10% at exit. To return 100x, you need a $1B exit.

To reach a $1B exit: assuming a 10x revenue multiple, you need $100M in annual revenue.

To reach $100M in annual revenue, you need to be operating in a market of at least $1B, because even the best companies rarely capture more than 10% of their market.

That's the chain. Billion-dollar market → $100M revenue → $1B exit → 100x return → 3x for the LP.

And these days, with valuations inflating, many VCs are asking for $10B markets, not $1B. The math is the same, just scaled up.

One more thing worth saying bluntly: success in a small market is failure, at least from a VC's perspective. If you build something genuinely excellent, but the ceiling of your market is $50M in total revenue, your investors don't make money. That's not a venture outcome.

Another way to think about it is this: if you're going to spend the next ten years building something, would you rather build a Lego house or the Empire State Building?

That's really what market size comes down to. You're choosing the scale of the opportunity you'll spend years pursuing. A smaller market doesn't mean you can't build a great business. It just means the ceiling is lower.

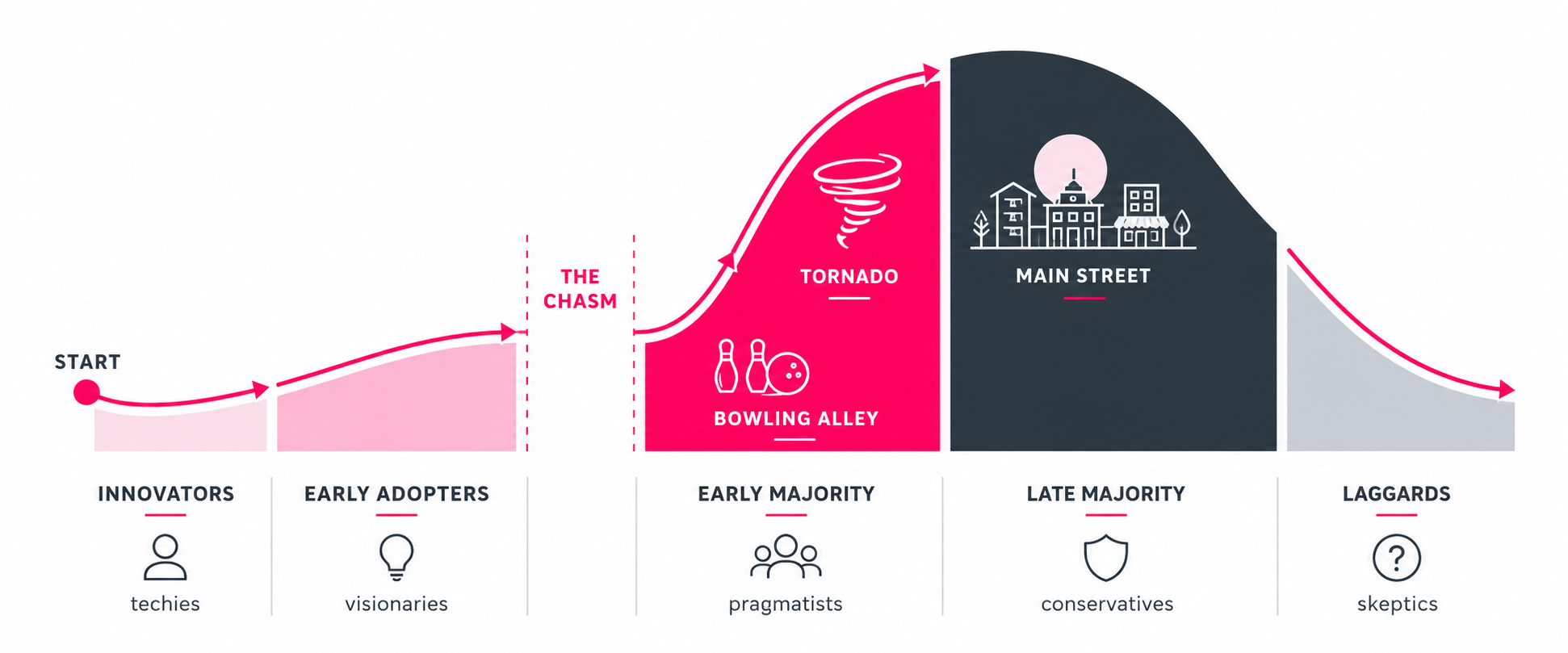

VCs want a market that's growing fast

Here's the dimension most founders forget: growth rate.

A static billion-dollar market is okay. A billion-dollar market growing at 30% per year is a completely different opportunity.

The concept VCs use here is CAGR: Compound Annual Growth Rate.

A double-digit CAGR is generally seen as a green flag. What investors are really looking for is a market about to enter what's called a tornado phase: the period when a technology moves from early adopters to the mainstream majority, and adoption spikes hard.

Think about how fast cars replaced horses. Or how quickly smartphones erased the market for point-and-shoot cameras. When a market enters that phase, rising tides lift all ships. If you're positioned there, you grow 20% per year just because you exist.

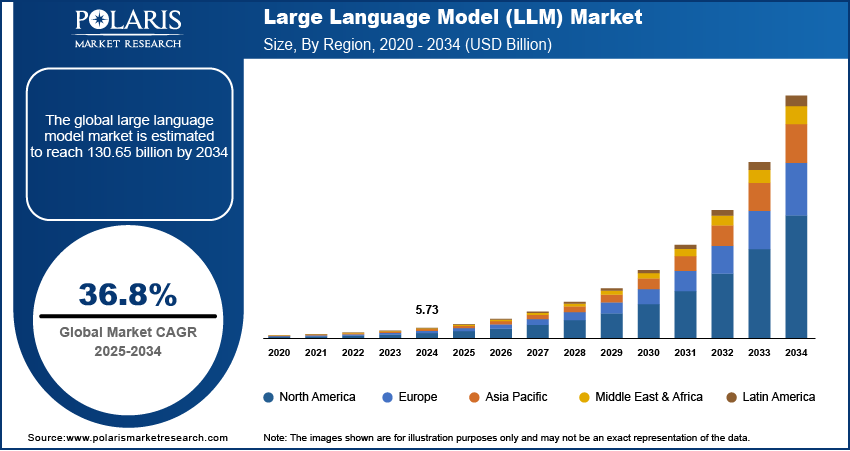

A recent example: the LLM market is projected to grow at roughly 37-40% per year through 2034. If you've built a half-decent product in that space, you're going to do well almost regardless of execution, because the market is doing a lot of the work for you.

Growth rate belongs on your market slide. If your CAGR is strong, put it there and explain what it means.

Find your ideal investors now

Browse 16,000+ investors, share your pitch deck, and manage replies - all for free.

Get Started Now

2. How to Calculate Your Market Size

Start with a clean definition

Market size has two clean definitions, and they're basically two sides of the same coin.

Definition 1: How much money you could earn in one year if every single potential customer in your market bought from you.

Definition 2: The total revenue of all your direct competitors combined.

Both lead to the same number.

By the way, market size is always expressed in monetary value, like dollars, euros, whatever currency applies.

Not number of users. Not units sold. MO-NEY.

Investors want to see a dollar figure. (Or euros, you get the idea).

Bottom-up market sizing: this is what VCs actually expect

Bottom-up is the standard. It's how serious founders do it, and it's the only method that will hold up under scrutiny.

The formula is simple: Number of units of demand × Revenue per unit = Market size

That said, getting to those inputs requires a bit of thought.

First, define your unit of demand. That depends on your business model:

- SaaS : Your unit is a customer or account. Your revenue per unit is ARPA (average revenue per account) or ARPU (average revenue per user).

- Marketplace : Your unit is a transaction. You earn a percentage-your take rate-of the gross merchandise value (GMV).

- Fintech : Same logic as marketplace. You have gross transaction value (GTV), and you take a cut.

This is why I always recommend building your business model slide before your market slide. The market slide is a direct extension of the business model. If you know what you charge per unit, you can multiply it by the whole market.

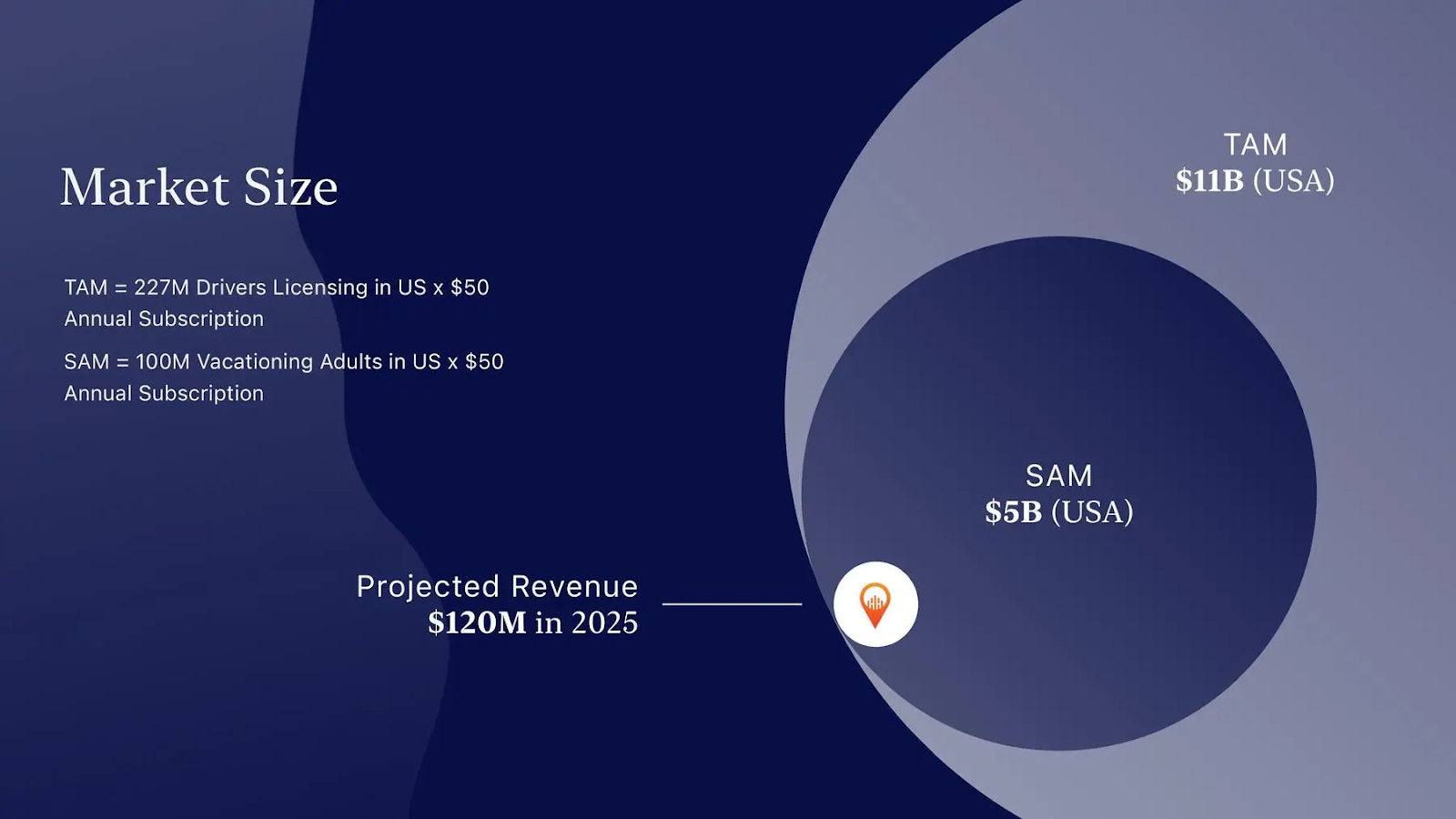

For example: if you're selling to vacationing adults in the US, and there are 100 million of them, and you're charging $50 per person per year, your market is $5 billion.

Simple. But you have to do the work to get those inputs right.

Top-down market sizing: how lazy founders get caught

I'm going to be direct here. Top-down market sizing is what you do when you haven't done your homework.

It looks like this: you Google "global mobile app market," find a Statista or Gartner report saying it's worth $200 billion, and drop that number into your deck.

That's wrong. And experienced investors will spot it instantly.

The problem isn't just that it's lazy. It's that it almost always leads to inflated numbers. If you're building a mobile app to help people learn English, your market is not "mobile apps." Spotify is a mobile app. Uber is a mobile app. Your market is English learning mobile apps, which is dramatically smaller.

Don’t do this:

A common version of this: a dental scheduling software startup claiming their TAM is "the global dental market at $500 billion." That number includes dental procedures, dentist salaries, equipment, real estate, and insurance. None of which you're selling. Your market is: number of dental clinics × annual software spend per clinic. That's it.

The trap this creates is "we only need 1% of the market." That phrase has become a red flag because it signals a top-down calculation. It's not factually wrong, but it's almost always a cover for sloppy math.

You can use top-down as a cross-check internally. It’s a sanity test to make sure your bottom-up number isn't wildly inconsistent with what industry data suggests. But the number you present to VCs should always come from the bottom up.

Value-theory market sizing: for new categories

Sometimes you're building something that doesn't have a comparable. There are no competitors, no existing market reports, because the category doesn't exist yet.

In that case, you work backwards from the value you deliver.

Here's the logic: if your product saves a customer 50 hours of work per month, and those people cost $20 per hour, you're delivering $1,000 in value per month. You then estimate what share of that value you can realistically capture as revenue. Maybe 20-25%. So you price at $200-$250 per month.

From there, you multiply by total potential customers, and you have a value-theory TAM.

It's less precise than bottom-up, but it's the right tool for genuinely new categories.

At the end of the day, the goal is to triangulate: run bottom-up, run top-down, run value-theory, and see if they land in the same ballpark. If they do, your estimate is credible. If they diverge wildly, you need to revisit your assumptions.

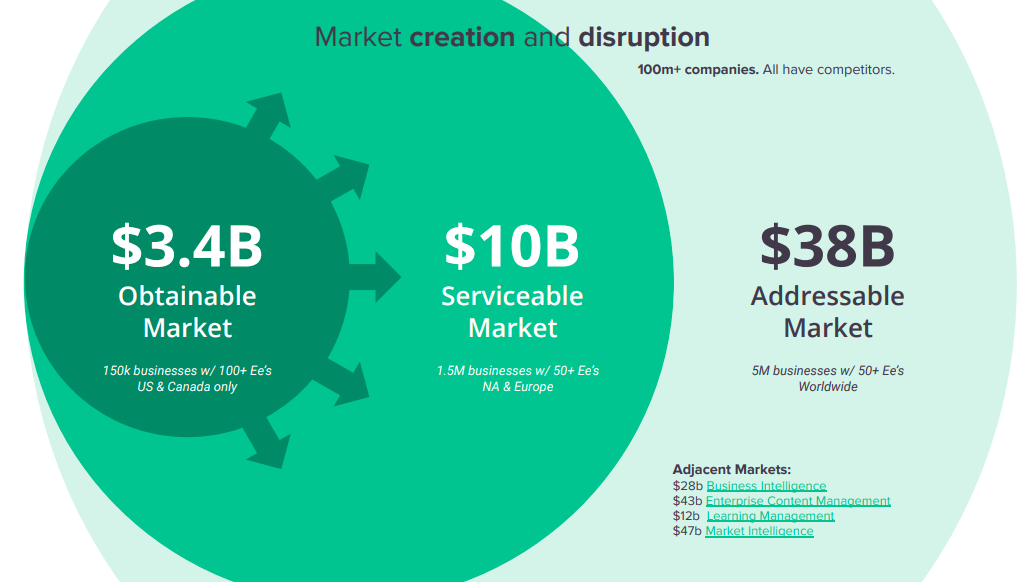

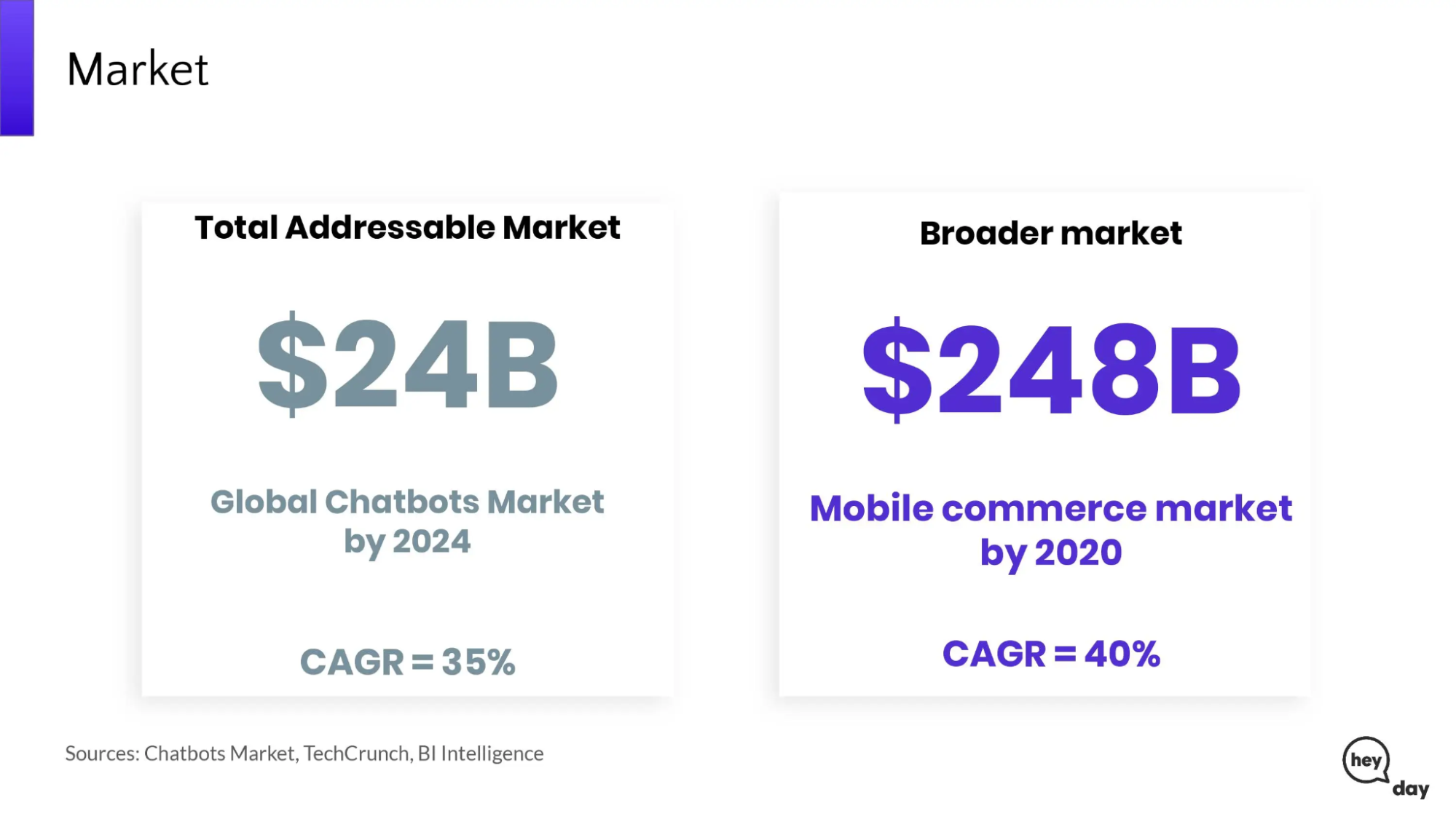

3. TAM, SAM, SOM: The Basics Nobody Actually Understands

Everyone uses these terms. Very few people know what they mean or calculate them correctly. Even some investors confuse them.

Here's the clean version.

TAM: The big picture

TAM stands for Total Addressable Market. It answers: how big could this market be in principle?

It's the annual revenue opportunity if you could serve every relevant customer globally. This is your largest number, and it's largely theoretical. It sets the ceiling (a reason for the investor to believe there's a big enough game to play).

SAM: The realistic opportunity

SAM stands for Serviceable Addressable Market. It answers: which part of that market can we actually play in?

This is where TAM gets filtered by reality. Not every potential customer is reachable. You might only sell in English-speaking markets. Your product might only integrate with certain systems. There may be regulatory constraints in certain geographies. SAM strips those out.

SAM is actually the most useful number in my opinion. It's not abstract like TAM, but it's not as granular as SOM. It tells you: this is the realistic upper bound of the opportunity in front of us.

SOM: The 3-5 year forecast

SOM stands for Serviceable Obtainable Market, or Share of Market. It answers: what revenue can we plausibly win?

Unlike TAM and SAM, which are strategic estimates, SOM is operational. It comes directly from your financial forecast. There's a spreadsheet behind it. It includes growth rates, headcount, CAC, conversion rates, and retention.

For pre-seed and seed startups, I'd build a 3-year SOM. Series B and beyond can push to 5 years. Beyond that, it's speculation.

Quick reference:

| Question it answers | Built from | |

| TAM | How big could this market be? | Market-level research |

| SAM | What can we actually serve? | TAM filtered by constraints |

| SOM | What will we realistically capture? | Financial forecast |

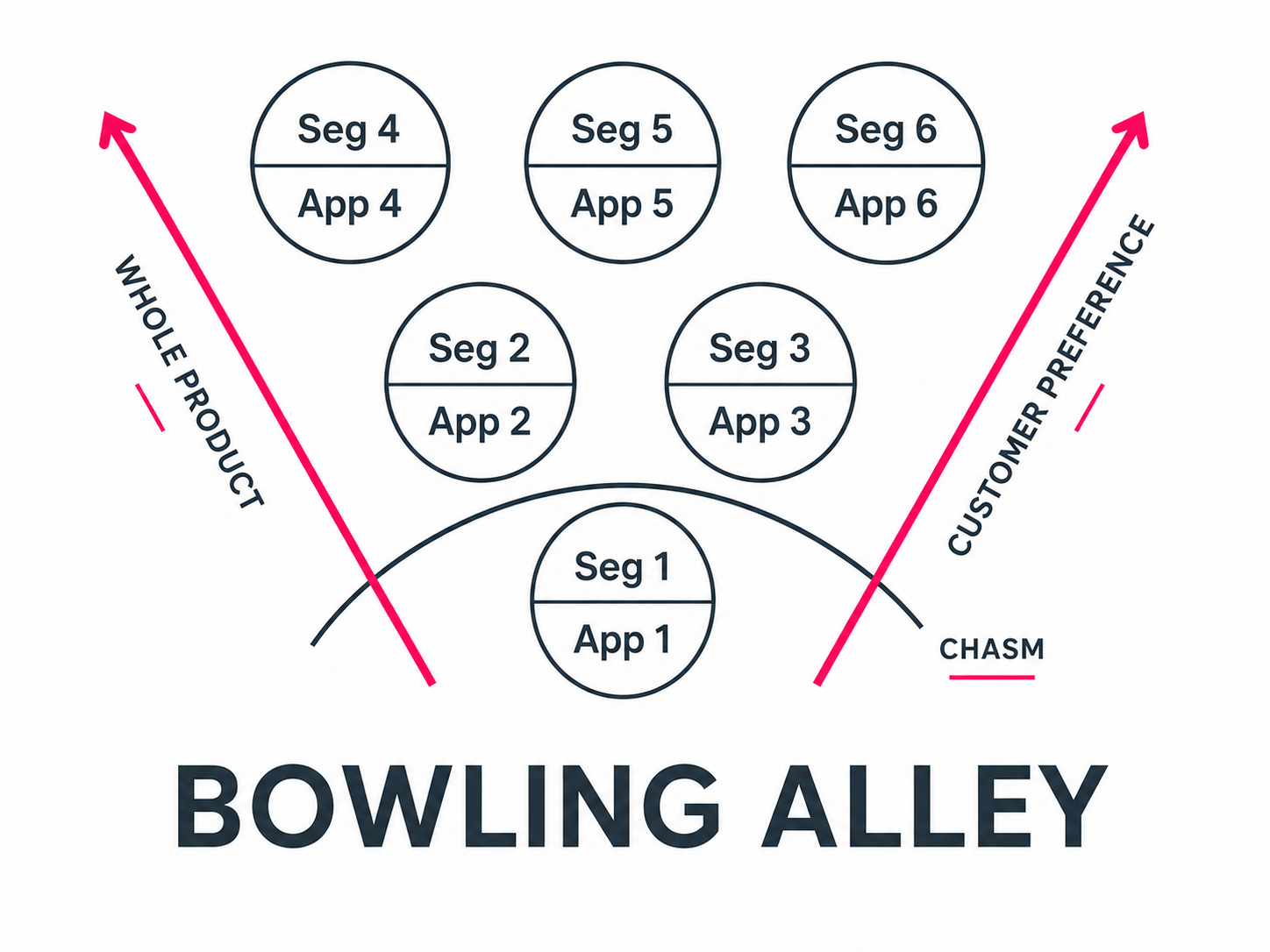

4. Market Penetration: Start Small, Think Big

"Start small, think big" isn't just some motivational phrase. It's a strategic playbook with real academic grounding.

The underlying framework comes from Geoffrey Moore's book Crossing the Chasm. He calls it the bowling alley theory.

The idea: you pick one narrow market segment as your starting point. You own it completely. Then you expand to an adjacent segment, carrying your brand credibility and operational experience with you. Rinse and repeat.

Each pin you knock down makes the next one easier. That's how you get from a niche entry point to a large market.

Your TAM, SAM, and SOM should reflect this thinking. They should tell the story of how you move from where you are today to where you could be.

Six real examples of how this plays out - with their original homepages for a little trip down memory lane :)

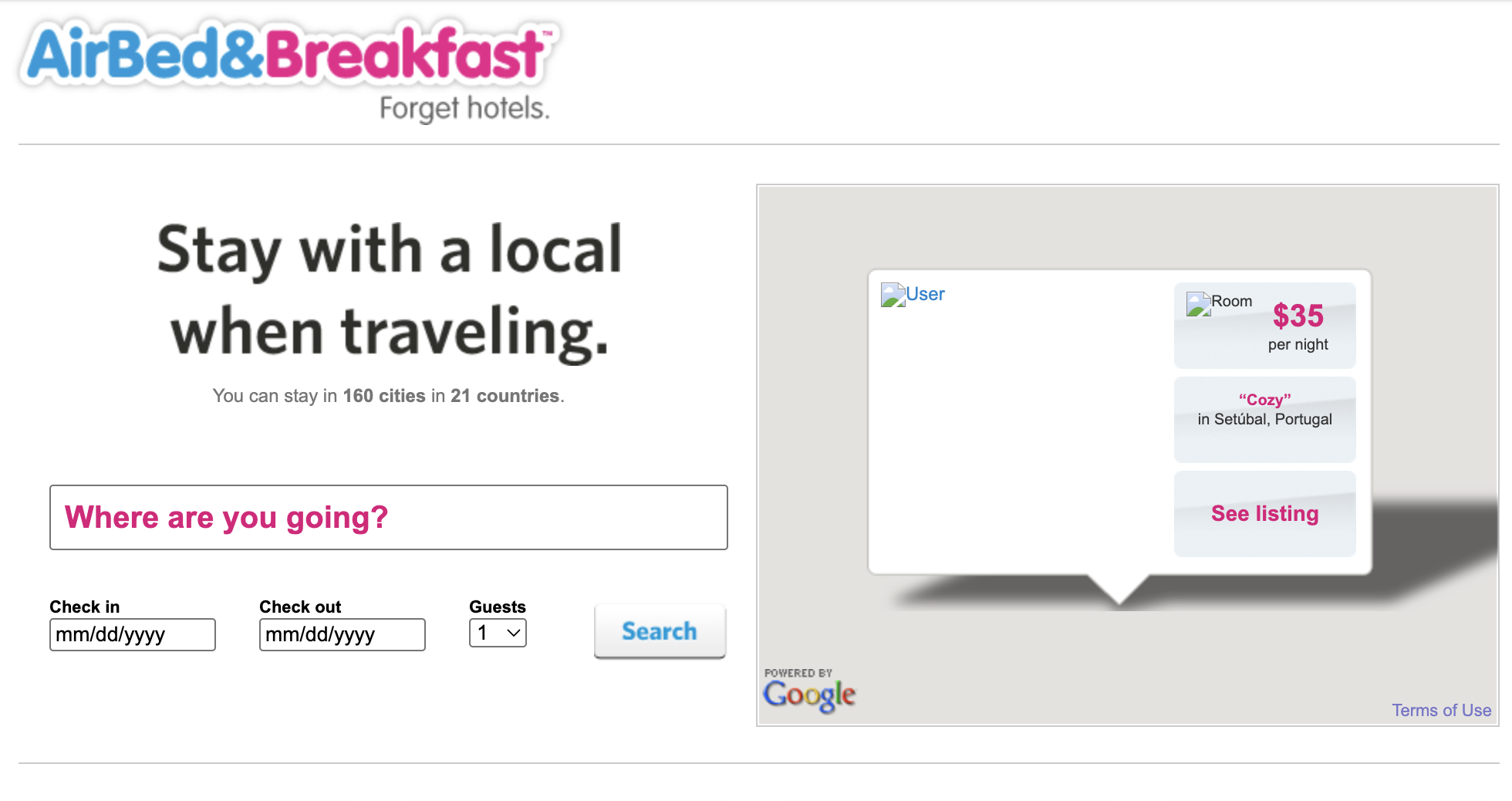

Going upmarket - Airbnb started with cheap, awkward air mattress rentals and is now offering luxury stays in the $1,000-per-night range.

Going downmarket - Tesla launched with the Roadster (a $100K+ sports car), then moved to increasingly affordable models targeting mass-market consumers.

Geographic expansion - DoorDash built density in suburbs and underserved US cities before expanding to major metros. Counterintuitive, but the unit economics worked better there. Their competitors went big cities first-and struggled.

Product segment expansion - Amazon started with books, then electronics, and eventually became "the everything store."

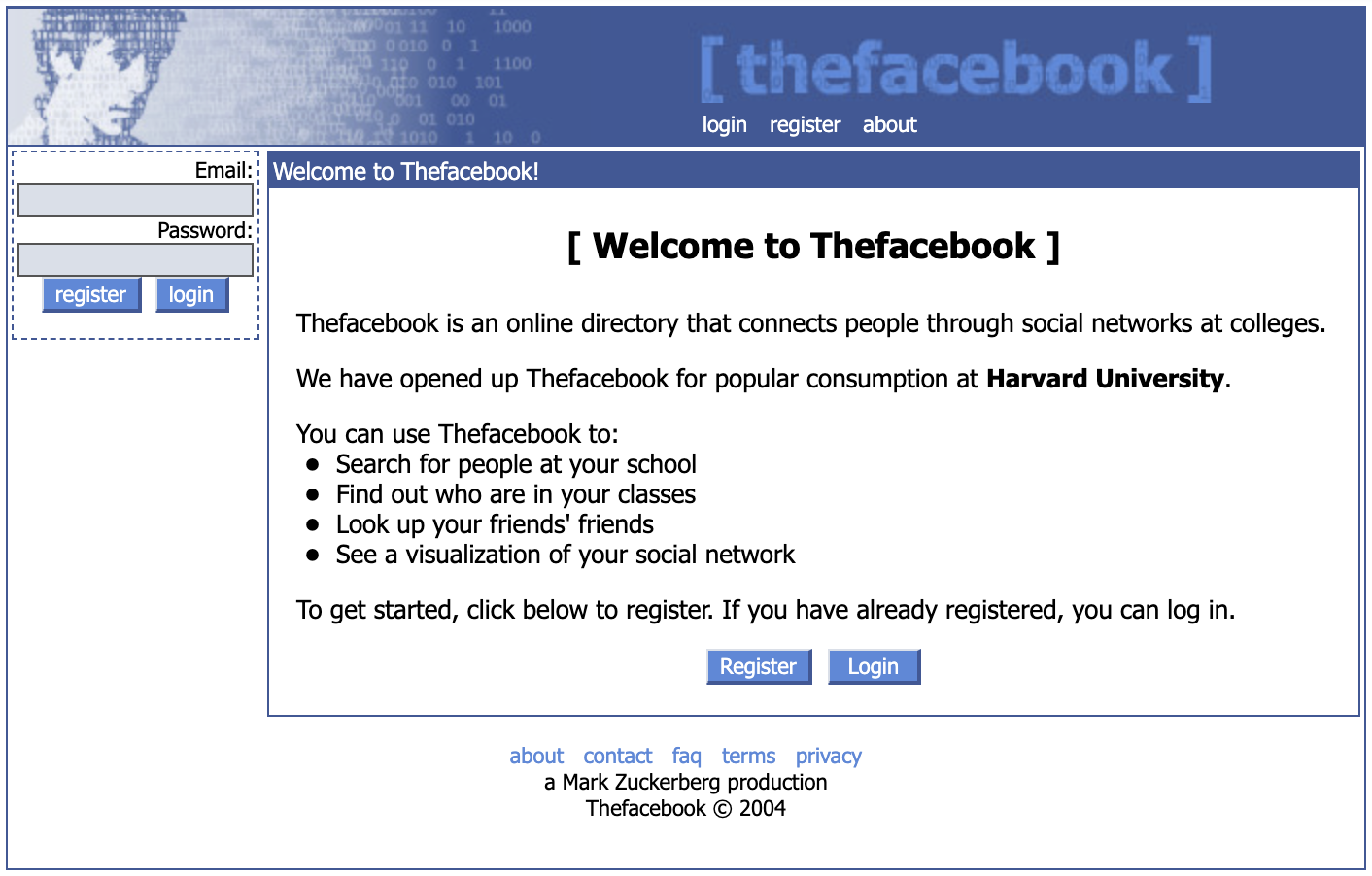

User segment expansion - Facebook launched at Harvard, then Ivy League, then US students broadly, then all students, then everyone.

Feature expansion - HubSpot launched as a marketing tool, then added a sales suite, then an ops suite. You start paying $20/month and end up paying $5,000/month because your whole business runs on it.

The point is to have a plan for how you move from pin one to pin two to pin three. Investors want to see that thinking reflected in how you construct your TAM, SAM, and SOM.

5. Demand Creation: Why Everyone Can't Be Uber

There's a concept worth understanding, and being careful about: demand creation.

Uber is the poster child of this. In 2010, New York City had about 180 million paid car trips per year. By 2019, that number was 420 million. More than doubled. But the population barely moved from 8.17 million to 8.34 million, according to US Census data.

Uber didn't just take riders from traditional taxis. It unlocked people who never would have ordered a taxi because the experience was too inconvenient, too opaque on pricing, or just not accessible. The product created new behavior.

That's real. Demand creation happens.

But here's the problem: you cannot credibly claim demand creation at the idea stage, before you have any data. When a pre-product, pre-revenue founder says "we'll create a whole new market," investors hear "I don't have real numbers."

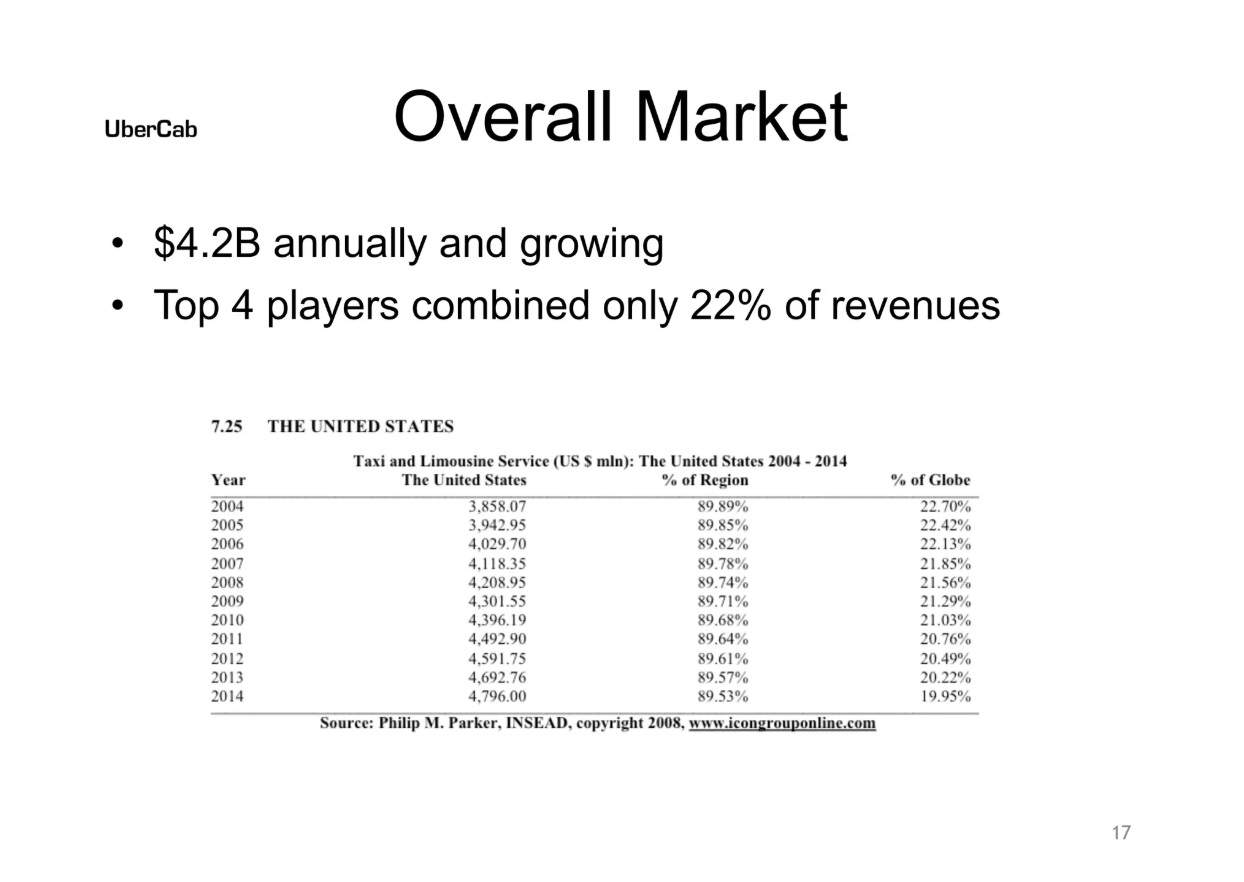

By the way, here's Uber's own market slide from their 2008 round. See for yourself:

Maybe you will unlock latent demand. Maybe your product will be genuinely transformative. But if you say so with nothing to back it up, you sound delusional, even if you turn out to be right.

My advice: build your market sizing on existing demand. Be conservative. If you've already got early traction that suggests demand creation, mention it and show the data. Otherwise, leave it out.

Market sizing is about credibility. How you say something matters as much as what you say.

6. Market Sizing Examples

Let's make this concrete.

Example 1: B2B SaaS for dental clinics

A startup sells patient recall and scheduling automation to dental clinics. They charge $300/month per clinic ($3,600/year).

- TAM : 200,000 English-language dental clinics × $3,600 = $720M

- SAM : Only 80,000 clinics are compatible with current integrations and in target geographies (US, UK, Canada, Australia, NZ) → 80,000 × $3,600 = $288M

- SOM : 5-year plan targets 5,000 clinics → 5,000 × $3,600 = $18M (6.25% of SAM)

That SOM is credible only if the go-to-market plan supports it: known conversion rates, sales capacity, CAC, and retention data.

Example 2: Marketplace for used lab equipment

A startup operates a used laboratory equipment marketplace with a 10% transaction fee.

- TAM : $4B GMV × 10% take rate = $400M

- SAM : Serving only North America and Europe (certified categories only) → $1.5B GMV × 10% = $150M

- SOM : 5,000 transactions/year × $12,000 avg. value × 10% = $6M (4% of SAM)

Note: for a marketplace, your market size is your revenue, not the GMV. Founders often make the mistake of presenting GMV as their TAM. It's not. It's the gross flow of transactions, not what you earn.

Example 3: AI copilot for financial institutions

A startup sells an AI compliance copilot to mid-market banks, credit unions, and fintech companies. Because this is a new category, most institutions don't have a dedicated AI budget yet. You need value-theory to cross-check your numbers.

Bottom-up approach: 4,000 target institutions × 20 eligible users × $2,000/user/year = $160M TAM

Value-theory cross-check: The product saves one FTE of compliance work per institution.

- Average compliance FTE cost: $120,000/year

- Realistic price capture: 25%

- Implied ACV: $30,000

4,000 institutions × $30,000 = $120M TAM

Bottom-up suggests $160M. Value-theory suggests $120M. The range is tight enough to be credible.

- SAM : 1,200 serviceable US institutions × $30,000 = $36M

- SOM : 3-year plan of 150 institutions × $30,000 = $4.5M

These numbers are probably too small to excite a VC, which brings us to the final point.

Market Size Is Necessary. It's Not Sufficient.

A weak market kills your raise. But a strong market doesn't guarantee one.

Here's the thing most founders miss: your market size is not yours. Any team building the same type of product can claim exactly the same TAM, SAM, and market growth rate as you. It's an external factor.

So do your homework. Know your numbers. Build a proper market slide so the analyst can tick their box. But don't lead with market size as your strongest argument, because any competitor can use the same slide.

What you own is everything else: your insights, your team, your distribution, your early traction, your unique approach to the problem. That's what makes the investment yours to win.

Market size opens the door. What's behind it is up to you.

Managing your fundraising process is another challenge entirely. OpenVC gives founders a searchable database of verified early-stage investors, a fundraising CRM built specifically for startups, and pitch deck tracking with per-investor engagement analytics - all in one place, free to use. If you're actively raising, it's worth a look.

Find your ideal investors now

Browse 16,000+ investors, share your pitch deck, and manage replies - all for free.

Get Started Now

![12 Best Startup Financial Model Templates [Free & Paid]](https://d1pnnwteuly8z3.cloudfront.net/images/177302d9-3657-45b7-ac9d-acf801d83a74/1b029edf-43cf-4bd9-9e37-203f66bf426f.png)