The fundraising landscape in the Gulf Cooperation Council (GCC) region has rapidly evolved, positioning the region as a growing hub for startups and investors alike.

When compared to mature markets like the US and EU, the GCC offers unique opportunities driven by its distinct macroeconomic factors, trade dynamics, and extensive sovereign funding. With regional governments pushing for diversification away from oil dependent industries, there has been a surge in startup activity that has been largely backed by sovereign wealth funds, corporate investors, and strategic partnerships.

Through a comparative analysis, this report delves into the macroeconomic landscape, trade market activity, sovereign funding, and the startup ecosystem in the GCC, shedding light on the region's growing significance within the global investment landscape.

Table of Contents

The Rise of the GCC as a global economic hub

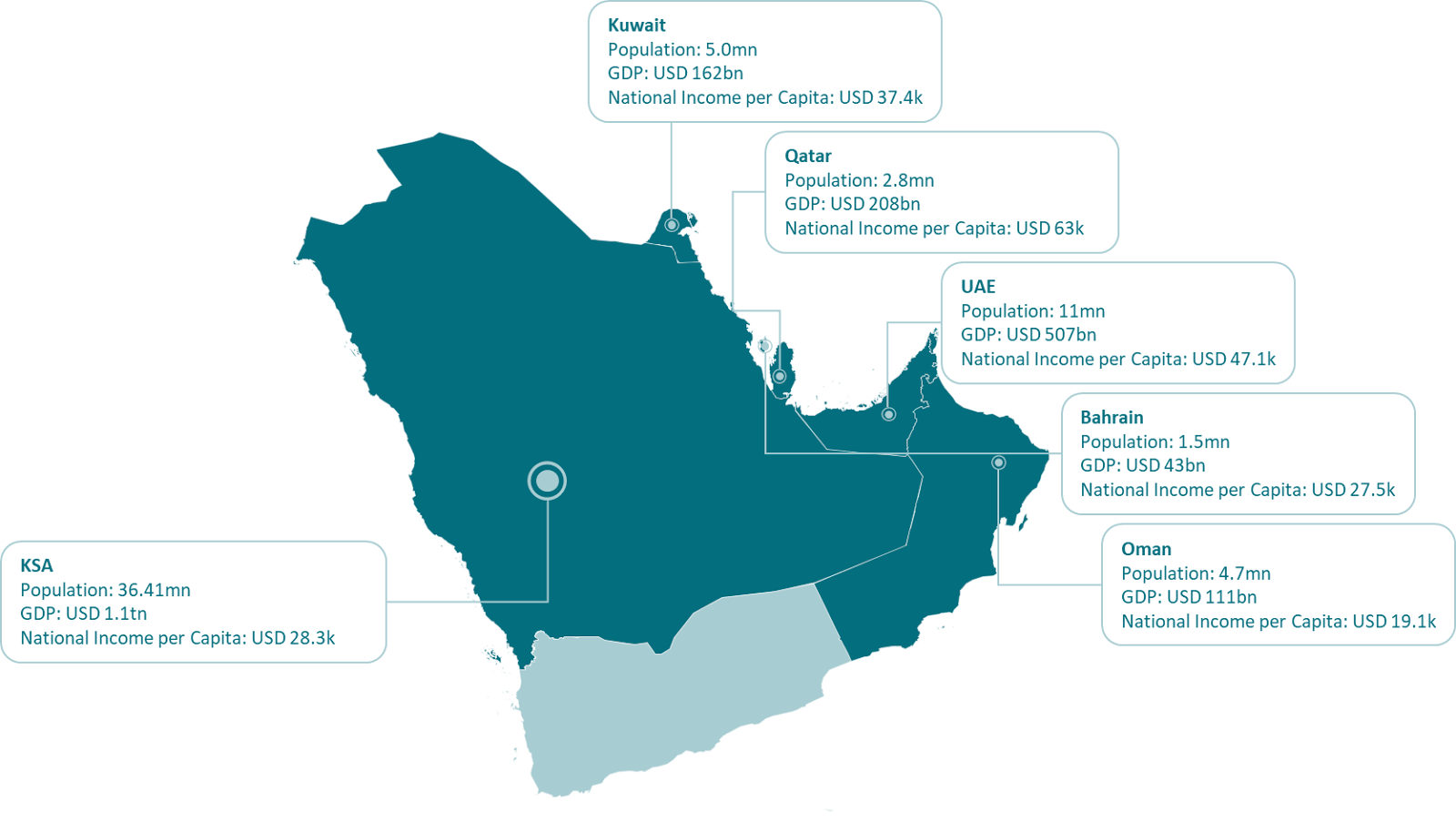

The GCC is a regional intergovernmental, political, and economic union that includes six Arab countries: Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, and the UAE. The union is governed by a charter that was signed in 1981.

The economic comparison between the GCC, US, and EU highlights notable economic trends. The GCC countries hold a smaller collective GDP, occupying 8% of US and 12% EU GDP in 2023, respectively. However, the region has experienced a steady growth, with GDP increasing from USD 1.7tn in 2018 to USD 2.3tn in 2023 – recording a 5-year CAGR of 6%, which is fairly in line with the US GDP growth and exceeds the EU GDP growth.

*GCC Countries Include Saudi Arabia, UAE, Qatar, Kuwait, Oman, Bahrain; EU Countries Include: Belgium, Bulgaria, Croatia, Cyprus, Czech Republic, Denmark, Estonia, Germany, France, Finland, Austria, Hungary, Finland, Greece, Ireland, Italy, Latvia, Lithuania, Portugal, Spain, Sweden.

Saudi Arabia stands as the largest contributor to the GCC's GDP, being the largest oil exporter in the region with oil and gas sectors accounting for 42%-50% of GDP; hence, fluctuations in oil prices have a significant impact on the country’s overall economic performance. Furthermore, KSA’s Vision 2030 initiatives, such as NEOM and the expansion of non-oil sectors, have been essential in broadening the country’s economic base. UAE also stands as the second largest contributor to the GCC’s GDP, fueled by the country’s strategic location and world-class infrastructure, making it a global hub for trade, logistics, and tourism. Finally, Qatar stands as the third largest contributor to the GCC’s GDP, with its GDP accelerating to occupy a larger share of 17% in 2023. The recent hike in the country’s GDP was mainly driven by (i) economic and infrastructure uplift following the 2022 World Cup, and (ii) increased LNG expansion, with LNG production expected to increase from current levels of 77 mtpa to 142 mtpa by 2030.

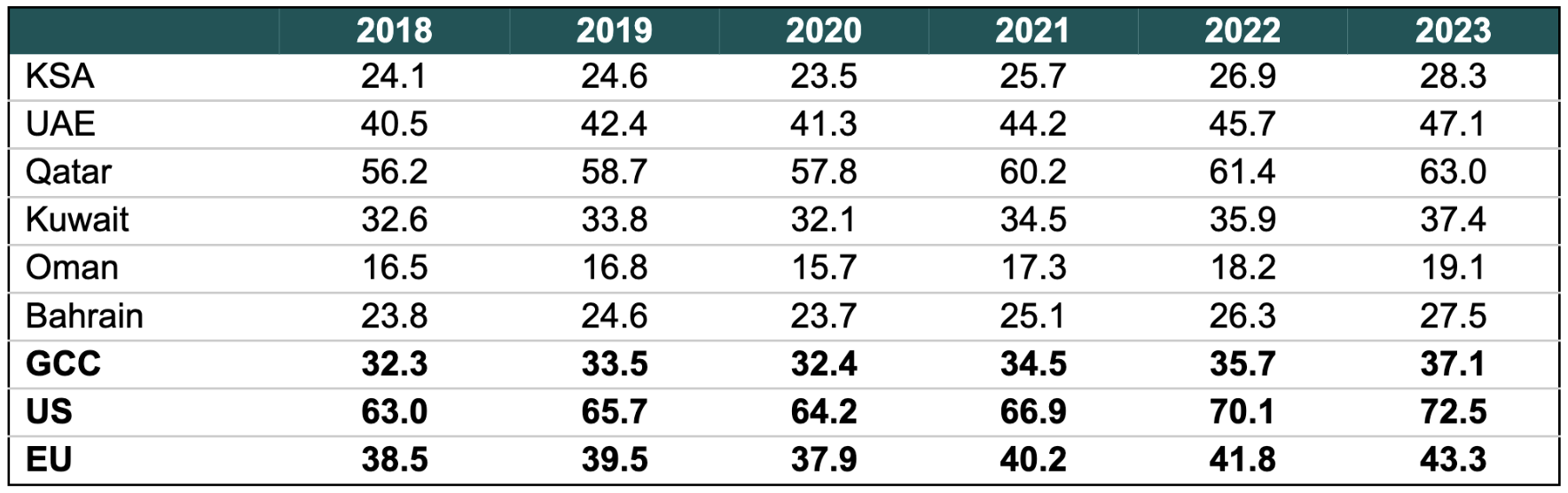

When assessing the national income per capita, the GCC shows a more dynamic trend compared the US and EU, rising from USD 32k in 2018 to USD 37k in 2023. Despite lagging behind the US and EU in absolute terms, the region holds a growing and comparable purchasing power, making it a great place for startups to grow their businesses. Qatar consistently ranks the highest in national income per capita, reaching USD 63k in 2023 (nearly double the average of the GCC region, and higher by 47% from EU) - mainly driven the country’s small population and substantial revenues from its highly developed oil and natural gas industries, which form the backbone of its economy.

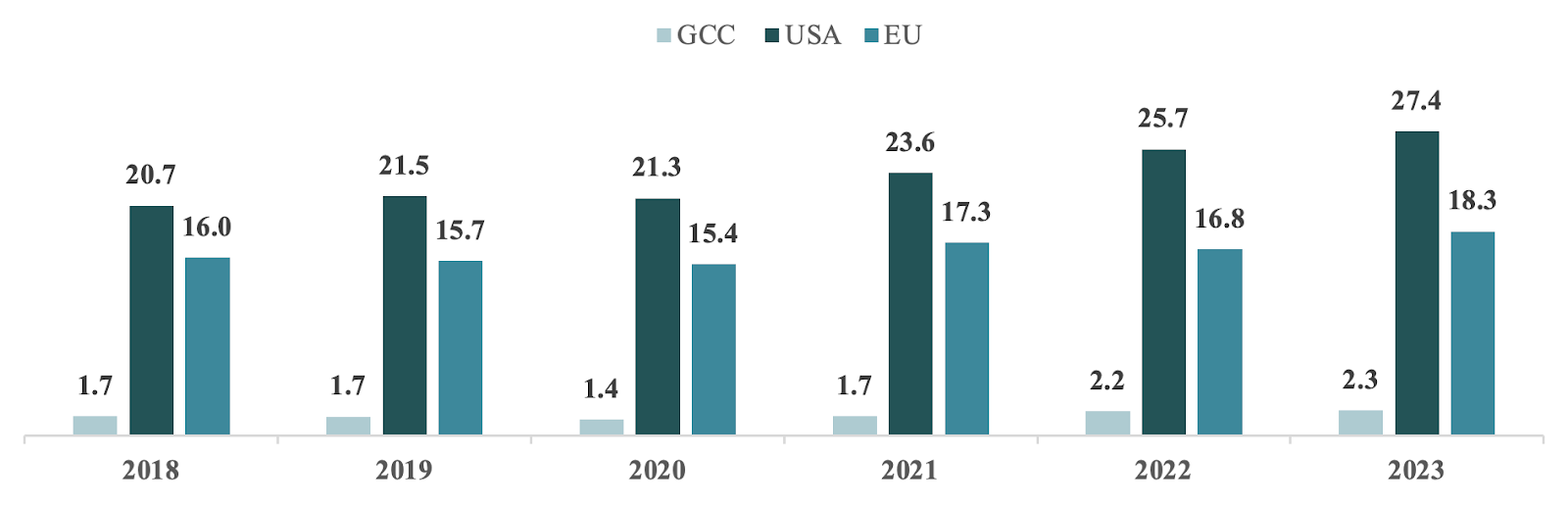

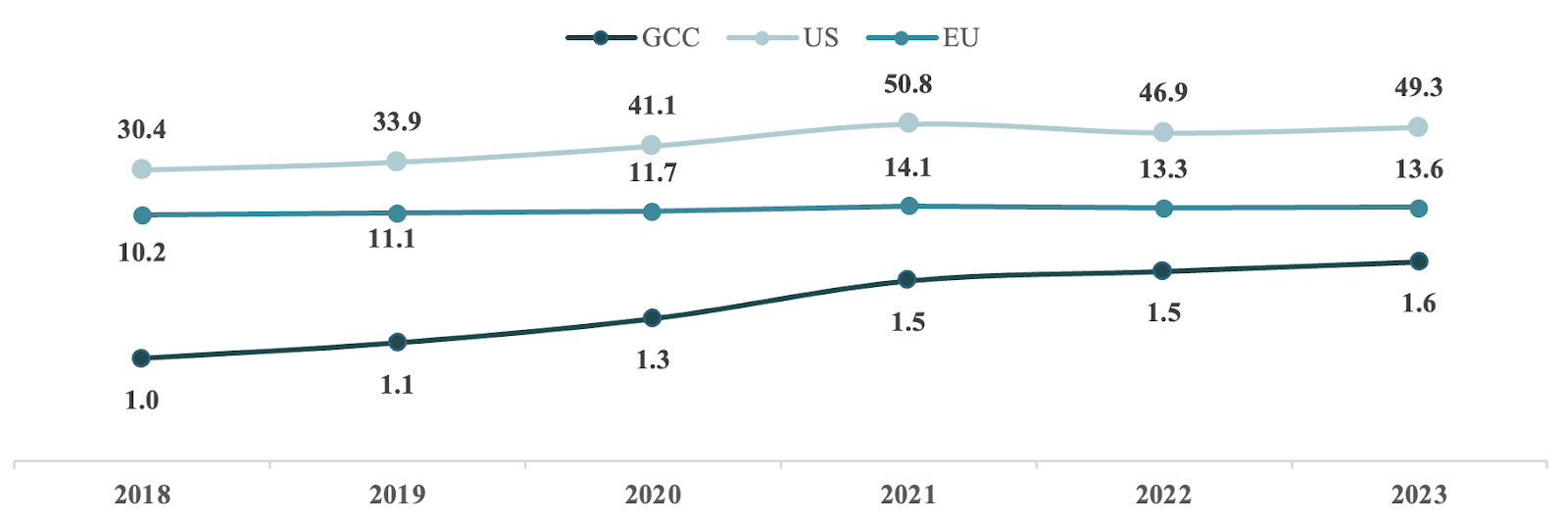

The global stock market size reached USD 109tn in 2023, of which the US occupied 45.0%, the EU occupied 12.4%, and the GCC occupied 1.4%. Despite its relatively smaller size, the GCC stock market demonstrated impressive expansion, growing at a 5-year CAGR of 8%, close to the US CAGR of 10% and higher than EU CAGR of 6%. This rapid growth can be attributed to economic diversification efforts, higher oil prices, and increased FDI in the region. Even though the GCC’s stock market is smaller than its Western counterparts in terms of market size, it has been showing signs of growth in recent years.

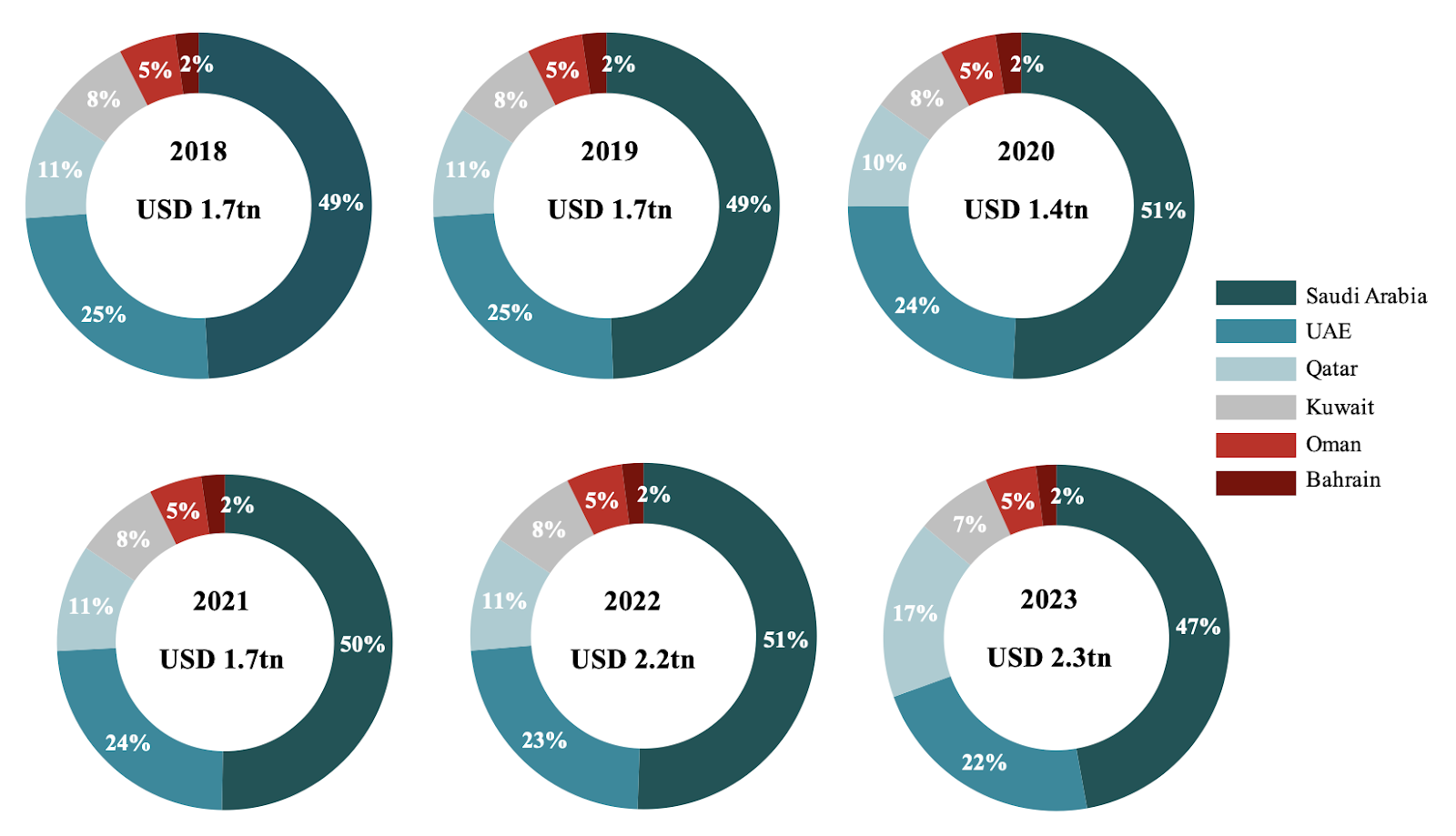

KSA leads the GCC in market size, with Saudi Aramco being the largest contributor to the region. Qatar and UAE follow in terms of market size, driven by large national companies like Qatar National Bank (QNB) and Etisalat respectively.

*GCC Stock Market Include Saudi Arabia, UAE, Qatar, Kuwait, Oman, Bahrain

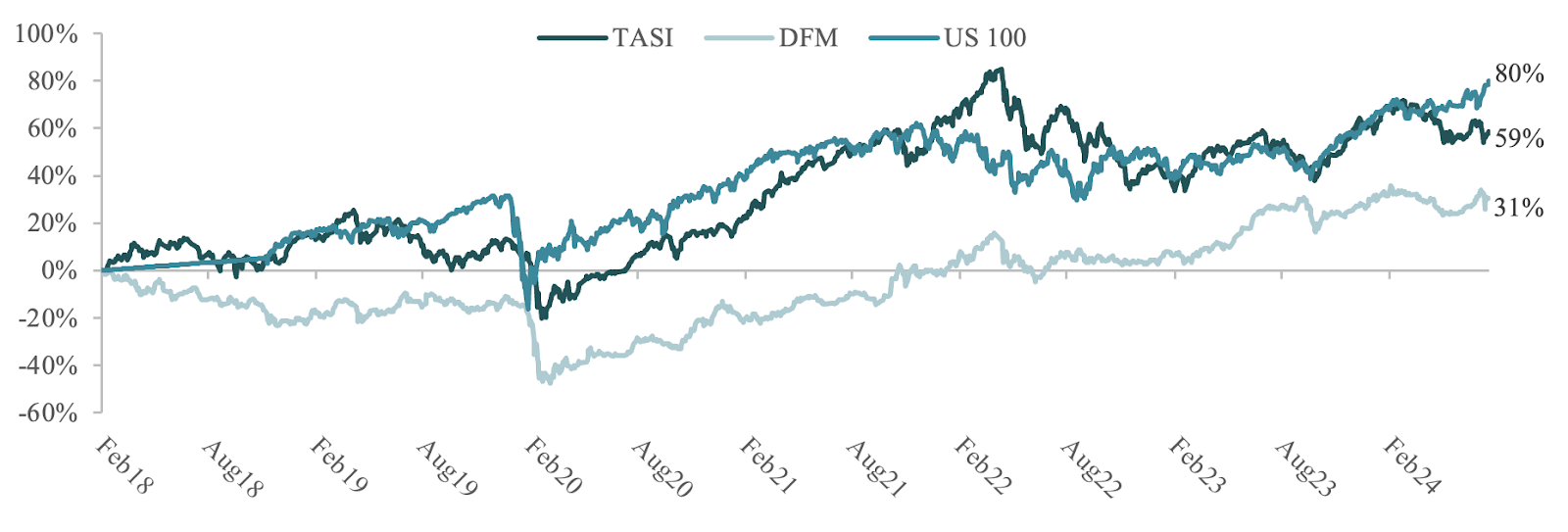

The Tadawul All Share Index (TASI), which represents the KSA stock market, experienced a sharp decline of c.20% in early 2020 mainly driven by the global economic downturn caused by the COVID-19 pandemic. However, by 2021 the index fully recovered, thanks to the stabilization of oil prices and the Saudi government’s ambitious economic reforms under Vision 2030. TASI has increased by 59% in 2024 to date, backed by the ongoing economic reforms and higher oil prices, both key drivers of KSA’s market recovery.

The Dubai Financial Market (DFM) has also declined by c.40%in early 2020 due to the pandemic, with slower recovery compared to TASI due to Dubai’s reliance on sectors like Real estate and Tourism, which took longer to recover post-COVID. DFM has increased by 31% in 2024 to date, but is still lagged behind TASI’s performance due to the slower recovery of its key industries.

Sovereign Funds Boost the GCC Venture Ecosystem

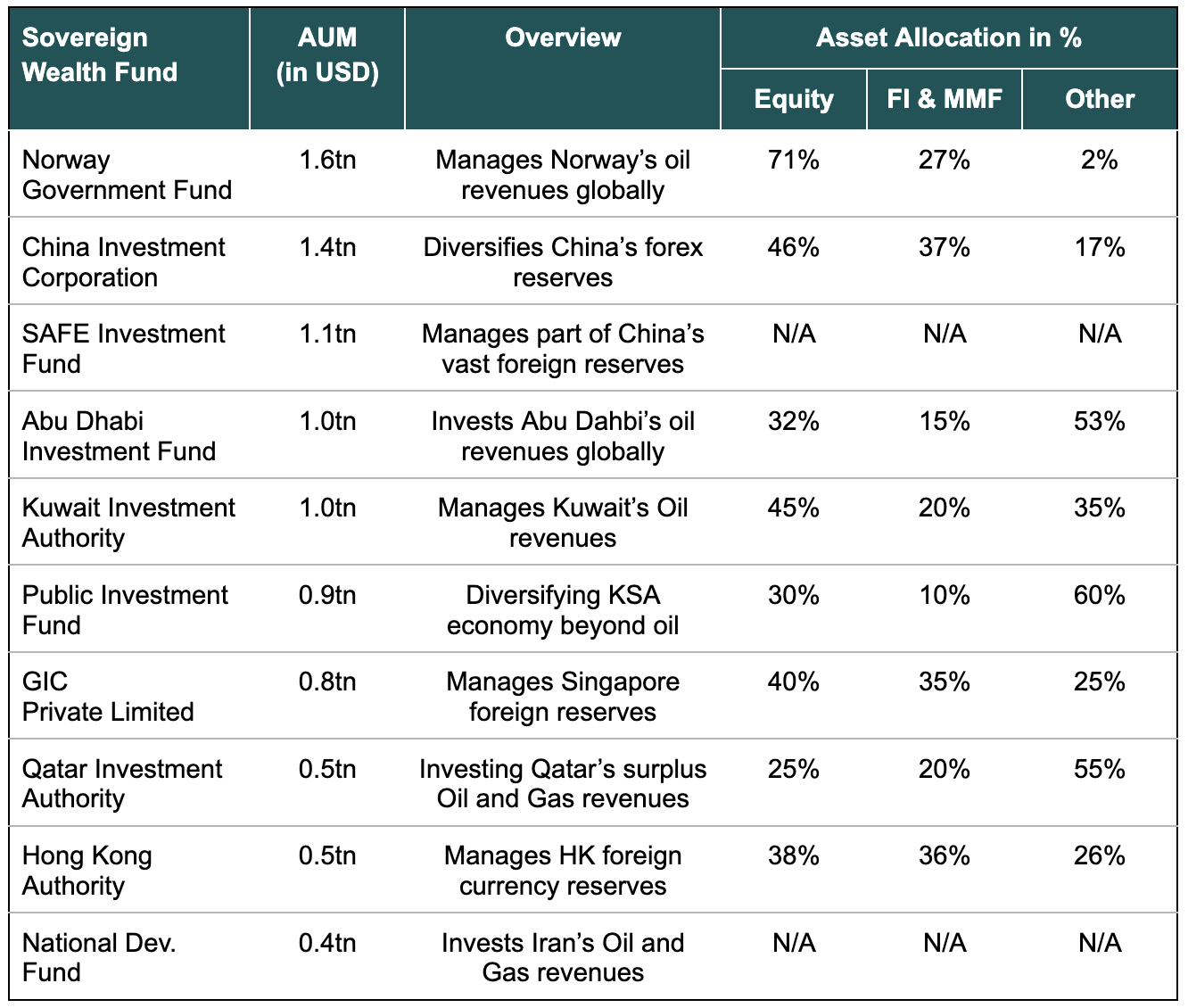

The investor landscape in the GCC is distinct from other developed markets, guided by explicit direction from central governments. Unlike the EU and US that predominantly feature organized private equity institutional investors as the main private capital sources, the GCC is spearheaded by family offices and sovereign wealth funds, which operate under the influence of governmental objectives. It is worth noting that the GCC holds 4 of the largest 10 SWFs in the world, highlighting the importance of SWF investment in the region.

Governments and sovereign wealth funds are actively seeking to unlock the potential value in assets like public utilities and former state-owned enterprises, which present appealing investment prospects for private capital. This interest in such assets not only increases the volume of transactions but also opens doors for private capital to engage in other business areas. Recently, private capital has ventured into government-controlled sectors such as oil and gas, exemplified by the sale and lease-back agreement involving Aramco Gas Pipelines Company with BlackRock and Hassana Investment Company.

In recent years, high-net-worth individuals (HNWIs) and families in the GCC have increasingly favored local investments due to fundamental factors like sustainable economic growth and an expanding customer base in the region. Opportunities have risen in various sectors, including the surge in e-commerce, tourism developments, and a heightened focus on renewable energy. Families traditionally resistant to third-party equity investments are now embracing private equity and initial public offerings as strategic avenues to institutionalize, accelerate growth, and diversify their wealth. The stabilization of oil prices, along with high-profile international events like Expo 2020 Dubai and the 2022 FIFA World Cup, have bolstered confidence among local investors. Furthermore, the GCC's geopolitical stability continues to prompt investors to retain their assets locally, perceiving them as safer amidst global geopolitical uncertainties.

Capital markets in the GCC have demonstrated notable outperformance, creating an attractive investment environment for all investors, including those in private equity and venture capital. Enhanced regulatory and governance frameworks, initiatives to boost liquidity in capital markets, and greater transparency have all contributed to increased investor confidence. Notably, the Middle East was one of only two global markets to defy the worldwide downturn in IPOs. In the first quarter of 2023, GCC stock markets generated USD 3.5bn from 12 IPOs. Additionally, GCC stock exchanges have seen heightened liquidity and trading volumes, providing investors with a wide array of investment opportunities across different sectors.

Startup Landscape in the GCC

The GCC’s VC and private equity landscape is rapidly evolving. The combination of active local and international VCs has created a fertile ground for startups and high growth companies. VCs like BECO Capital, Saudi Technology Ventures (STV) and Middle East Venture Partners (MEVP) have been active in the region for several years now, participating in the funding of many successful startups like Careem, SWVL, Anghami and Property Finder. Crowdfunding has also gained traction in the region. Platforms like Eureeca and Zoomaal, which allow startups to pitch their ideas and reach out to investors, have helped many startups raise funds from individual investors.

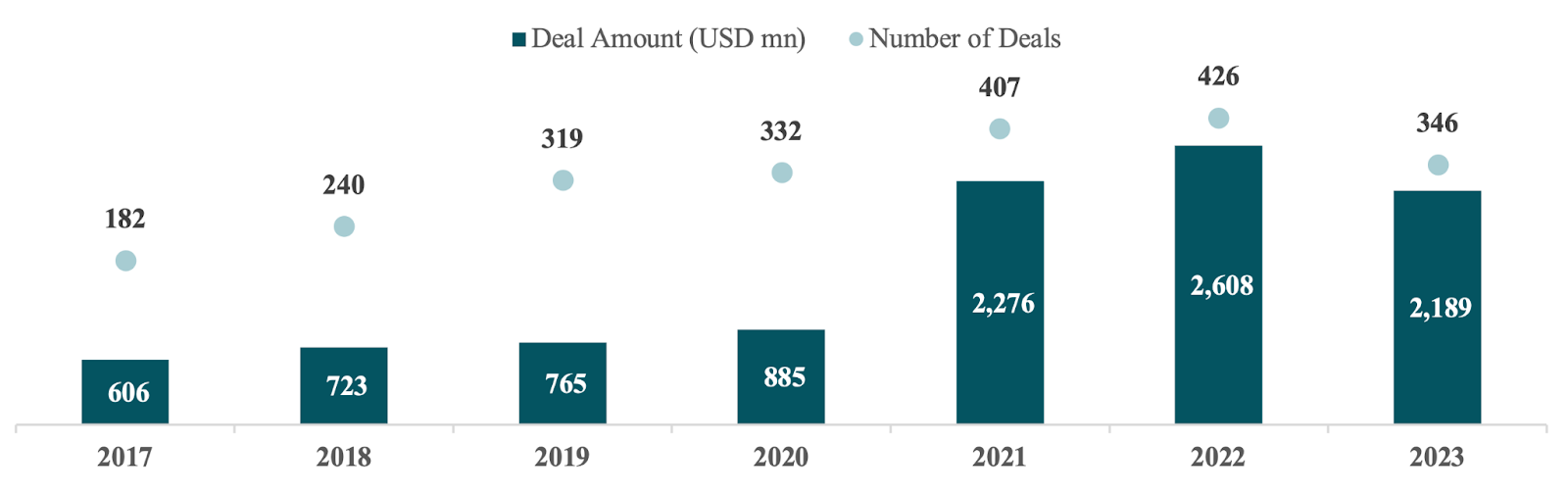

In recent years, there has been a surge in venture investments in the GCC, as capital invested grew at a CAGR of 24% over the past five years. From USD 606bn in 2017 to USD 2.1tn in 2023. This growth has been driven by funding startups that are headquartered in KSA and UAE. The drop in 2023 is due the economic uncertainties, changes in investor sentiment, and geopolitical tensions affecting the region. The Israel-Gaza conflict, along with other geopolitical tensions, contributed to the decline in venture investments across the GCC. Investor sentiment was negatively impacted due to increased uncertainty in the region, leading to a more cautious approach. Additionally, the global economic slowdown and rising inflation affected overall investor confidence, as did tightening monetary policies in key economies like the US and EU.

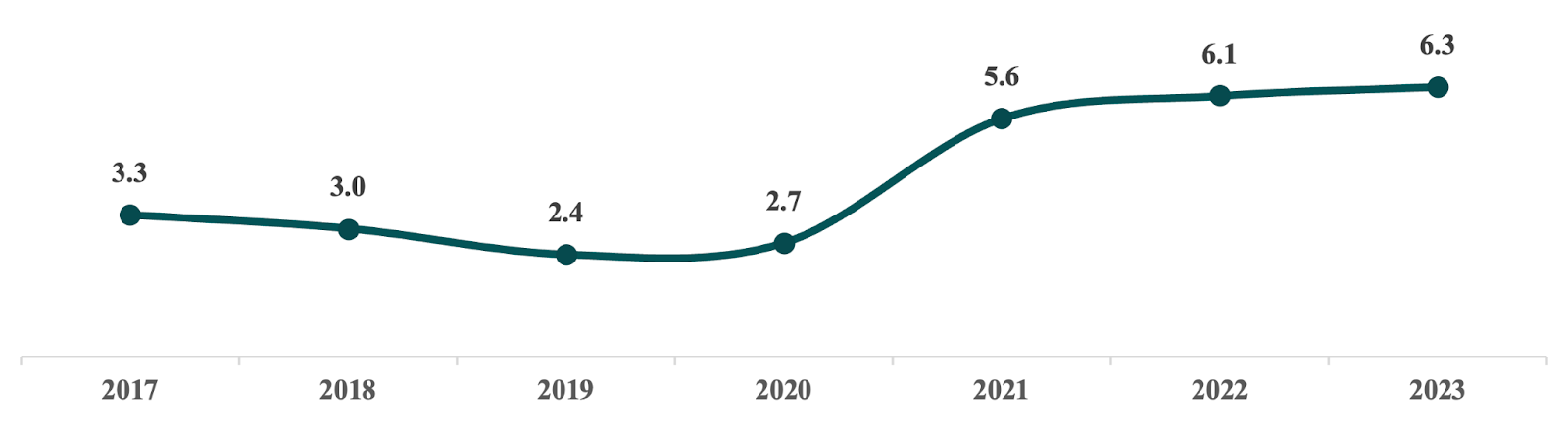

There has been a noticeable increase in venture investment in 2021 as markets stabilized and investor confidence returned post-Covid, particularly in the GCC which had, by that time, begun strategically diversifying its economy. Furthermore, the number of venture deals has more than doubled since 2017 and reached a peak of 426 in 2022. The average ticket of investment in 2023 was around USD 6.3mn, almost double that of 2017.

The growing startup environment in the GCC, encouraged by government initiatives that aim to attract innovative entrepreneurs, means that the region is expecting a boom in startups and SMEs. Sectors like healthcare and real estate are among the most attractive sectors, with tech expected to follow suit soon. Furthermore, by 2030, 45 unicorns worth an estimated USD 100bn are expected to emerge from the region.

Unicorns like Careem, Noon, Jahez, and Hunger Station have already proved that the GCC is the ideal platform for startups and technology companies to thrive. This is only just the beginning, and VCs will have a much bigger role to play in the GCC in the future.

Case Study: Careem’s Fundraising Success Story

One example of a startup that was extremely successful in the GCC, in line with making a positive impact in the community, is Careem. Careem is a Dubai-based ride-hailing company and was founded in 2012 by Mudassir Sheikha and Magnus Olsson. What started off as a web-based service for corporate car bookings quickly evolved into a full-fledged ride-hailing service addressing transportation challenges across the Middle East.

Careem’s journey from a startup to unicorn not only set a precedent for other startups in the region, but also highlighted the potential of the region as a fertile ground for tech innovation and startup investment.

This case study also shows that, while SWFs in the region are quite dominant, VCs and private investment are not non-existent in the region. There are many VCs and startup accelerators that have participated in notable deals in the GCC.

Conclusion

The GCC’s fundraising landscape is uniquely positioned at the crossroads of global trade and regional economic transformation. While the US and EU continue to dominate the global investment scene, the GCC's sovereign wealth funds and strategic initiatives offer compelling alternatives for investors seeking growth in emerging markets. The rise of regional success stories like Careem reflects the expanding startup ecosystem, with governments playing a pivotal role in providing both financial backing and regulatory support. As the region continues to diversify its economy and foster innovation, the GCC is set to play an increasingly important role on the global fundraising stage, offering a distinct landscape for startups and investors alike.

Unlock the secrets to startup fundraising 🚀

Use our FREE, expert-backed playbook to define your valuation, build VC connections, and secure capital faster

Get my playbook

About the author

Mirette Ramez is the Founder and Managing Director of Nexus Capital, a leading financial advisory firm in the MENA region. She has over a decade of experience in investment banking, private equity, and venture capital, with previous roles at Renaissance Capital, Egypt Ventures, and Tanmiya Capital Ventures. Mirette has led transactions exceeding USD 1B, including IPOs for Macro Group and e-finance on the EGX.

![12 Best Startup Financial Model Templates [Free & Paid]](https://d1pnnwteuly8z3.cloudfront.net/images/177302d9-3657-45b7-ac9d-acf801d83a74/1b029edf-43cf-4bd9-9e37-203f66bf426f.png)