People ask me all the time whether my time as a VC was helpful for preparing me to be a founder. Most of the time, I say ‘not really’. If I wanted to better prepare myself for being a founder, I would’ve been more prepared by working at an early stage startup or starting a startup before!

However, when it comes to fundraising, it’s my niche skillset’s time to ✨SHINE✨. Counter to the most common assumption, VC wasn’t that helpful for the connections to VCs (which can be replicated and made more effectively in other roles outside of VC in my opinion), but rather for understanding VC psychology when it came to term sheets and $$$$.

By the way, hi! I’m Steph - I’m the founder of PIN, a platform that does all the backend legal/admin/tax work so groups of people (including unaccredited people) can invest together in startups. Some of our biggest use cases are founders investing in each other, school and company alum investing in startups founded by their community members, and creators investing with their followers. Before PIN, I was a VC at NEA where I did seed through growth investing in tech startups of all sorts.

Here are some of the not-as-obvious insights about VCs/their incentives + goals that hopefully help founders get to better deals with the VCs they choose to work with.

Table of Contents

P.S. None of this is legal advice. 😬 Please don’t make me regret this.

Two things about term sheets to tattoo on your brain

Valuation doesn’t matter as much as the terms

Large valuations sound great. They’re an immediate dopamine hit. An amazing headline!! Bad terms seem harmless on paper, and even less so when they’re disguised in legal jargon and buried in 100 pages of docs that you may or may not have read. I’ve been there. However, if there’s one thing to take away from this, it’s that working with clean terms and good people is worth so much more than a higher valuation on paper.

This post by Janelle Teng gives insight into how on how $1b valuations can be created by trading for ‘dirty terms’. I’m also reminded of this story of the early Snap days and how super pro rata + veto rights impacted the founders’ control. Be warned.

There’s no better ‘trick’ to getting the valuation and terms you want than by having multiple term sheets

Multiple term sheets means you have more leverage and confidence when negotiating. Getting multiple, simultaneous offers is the best thing you can do to put yourself in a position of strength, and then use the below to help refine

How VCs think and how it impacts how they negotiate term sheets

Many VCs have ownership targets

If you’re talking to an established VC firm that typically leads deals, they likely want to own more rather than less of your company. Many VCs internally have an “ownership target” or ownership minimum that they require to invest in a deal. Depending on stage and the firm philosophy, this can be anywhere from 5 to ~20%+.

Why? VCs generally prefer owning more of fewer companies vs. owning less of a ton of companies. It’s less work (less individual companies to sit on the boards of/provide ~value add~ to, etc) and means that if one of their investments breaks out, they’ll have meaningful enough upside for the returns to make a difference to their fund.

What this means for you as a founder:

- How much you raise and how much % you’re willing to give away matters. For example, if you’re expecting a $100M post-money valuation but only raising $1M (and therefore only willing to give away 1% of your company), you’ll disqualify yourself from being considered by many VCs (even if they think the valuation is reasonable) because they would expect to own ~10% or more. Keep this in mind when answering the precious “how much are you raising?” question from VCs.

- The VC you’re talking to might care a lot more about ownership than they do about valuation (and therefore the amount of money they give you to earn more ownership). To take a very simple example, say you’re raising $1M, and you’ve already had $250K in commitments from angels/previous investors (meaning $750K is available for a new, lead investor). If that new lead investor were to invest that $750K at a $10M post-money valuation, they would own 7.5%, and you would be giving up a total of 10%. If that lead is interested in owning more, you could ask for a $12M post-money valuation where you’d still be open to taking the same 10% dilution (therefore raising a total of $1.2M instead of $1M). That scenario would allow you to take the $250K in commitments from angels and give the VC the remainder (950,000) which would net them a 7.9% ownership instead of a 7.5% ownership. They give you more capital (in this case, an extra $200K), but to a multi-million / multi-billion dollar fund, that tradeoff could be well worth it for them and their strategy.

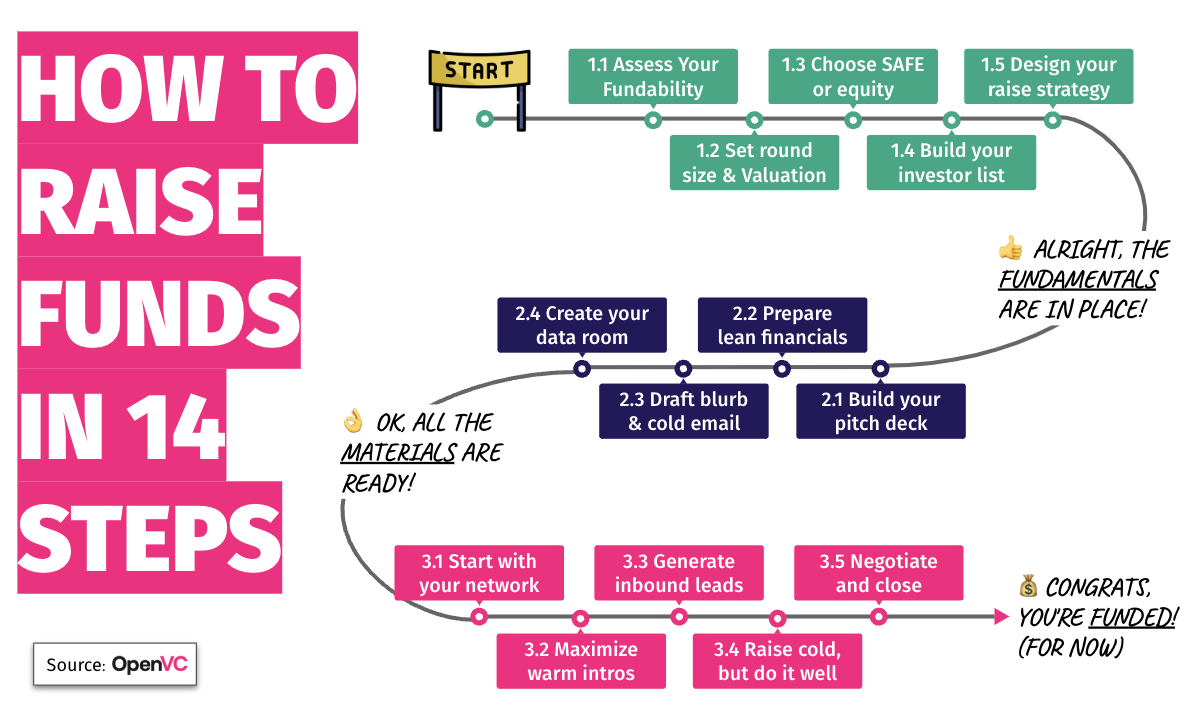

Unlock the secrets to startup fundraising 🚀

Use our FREE, expert-backed playbook to define your valuation, build VC connections, and secure capital faster

Get my playbook

VCs want the right people on the cap table

This couples closely with the above point - VCs want ownership and they usually want to take the vast majority of a round, but they also want the company to be successful. This means having special advisors/angels as equity holders is a good thing for the company, and therefore also in their best interests.

What this means for you as a founder: make a good case for how much of the round you want to leave open or allocate to who, and it could persuade your lead to come down on the amount they’re investing, or more likely, invest more at a higher valuation to preserve ownership but still make room for thee strategic investors.

VCs care about founders’ ownership

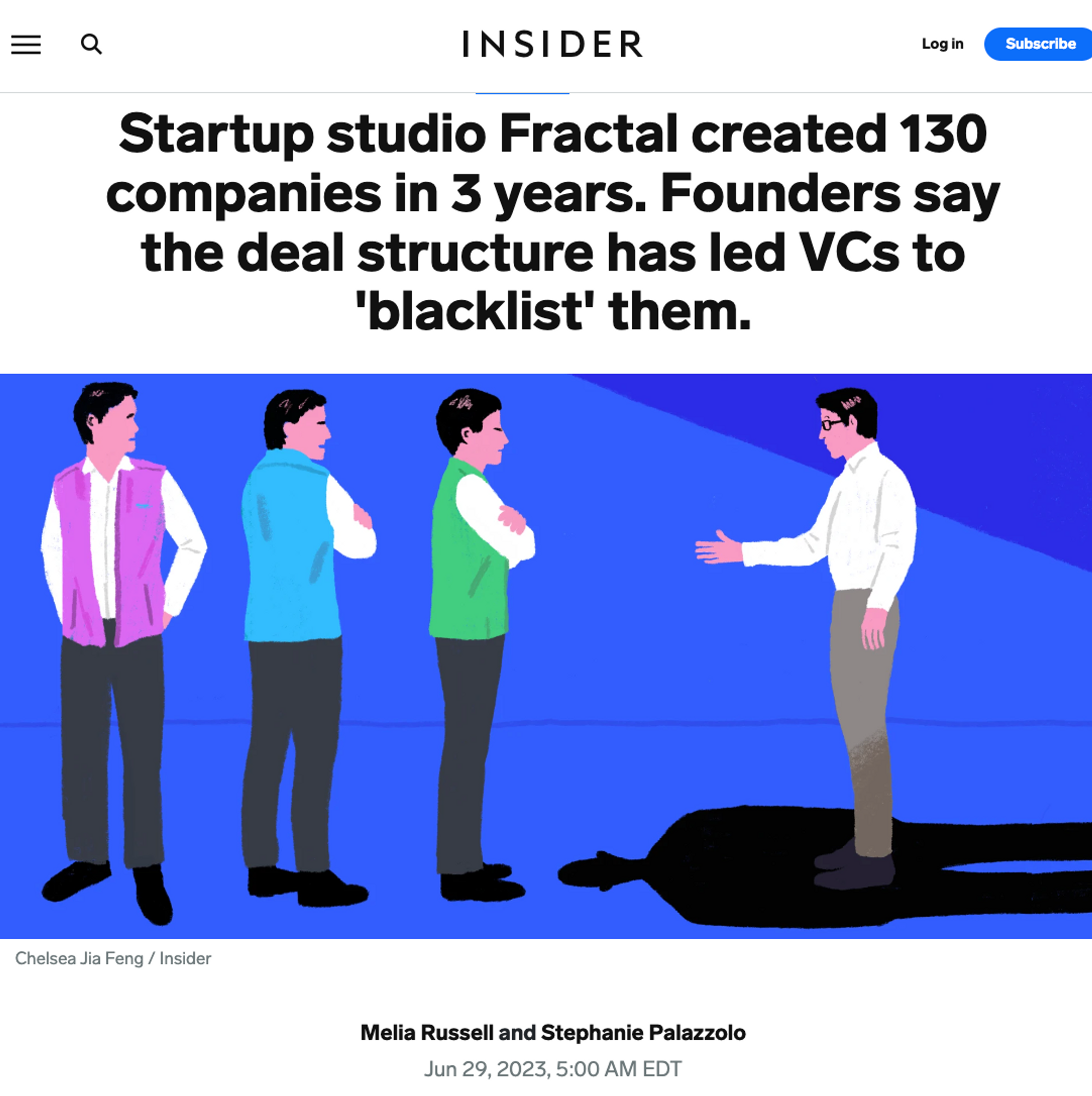

VC’s want ownership, but they know they’d be hurting the company if the founders themselves weren’t properly incentivized by having a meaningful ownership position themselves. (This is actually a big reason I’ve seen VCs pass on (many) incubated startups where founders typically have much less equity, but that’s a rant for a different time…).

Interestingly enough, the above article just came out and illustrates this point perfectly

What this means for you as a founder: most VCs don’t extract the most possible equity they can (unless they’re predatory, inexperienced, or short-sighted… which is why VCs who do this are instant red flags and I’d be extra careful about diligencing them because this is abnormal behavior 🚩🚩🚩). VCs want to maximize ownership but within reason, and want to be mindful of future dilution as well.

Don’t just ask for a valuation because it’s higher and better for you as a stakeholder. In my experience of negotiating, I emphasized a valuation target/range I was hoping for backed up by:

"I wanted to be mindful of dilution for myself but also for all stakeholders including early employees, taking into account money I had raised previously, other strategic angels/stakeholders I wanted to bring into the round, and because I knew future rounds over the lifetime of the company would further dilute everyone."

This was unnecessary, but as a chronic over-preparer who doesn’t like doing public math on the fly, I even had a very basic model that showed my cap table under different scenarios and outlined expected dilution from future rounds (assuming each had 5-15% ownership expectations). This probably didn’t move the needle that much, but reiterated the fact that I was thoughtful, thinking long-term, and incentive-aligned with the VCs I was speaking with.

The type and stage of VC firm impacts how they think about valuation

Different types of VC firms have different goals when investing at the early stage. For example, for seed stage companies, if you’re talking to a later stage VC, they might be ok with putting in a smaller check for smaller ownership and are typically less price sensitive. Putting in a small check of a few hundred thousand dollars is not going to move the needle on their multi-billion dollar fund even if (or rather, when 😏) you were to outperform, so this investment is less for the financial return and more for the option value. They want to stay close and invest in you later at the Series A or beyond where they’d put in $10M+.

This is very different psychology from seed firms, whose funds depend on each investment dollar. They’ll be more price sensitive, want reasonable ownership, etc.

What this means for founders: understanding how a specific VC is set up and therefore thinks about your investment will help you understand how important valuation and certain terms like pro rata rights are to them.

Some VCs, by culture/investing philosophy, are more valuation sensitive than others

Stage of VCs is a big driver of how they think about term sheet negotiation, but even VCs that invest in the same stage have very different views on terms and valuation.

I’ve noticed that, culturally, some firms are willing to pay to play - they invest at high valuations regularly because the partnership sees it as a necessary cost of getting into a competitive deal. The philosophy is that if they believe in a company, it’ll be wildly successful (and many multiples higher than what they’re investing at now), so the difference between a $10M, $20M, or $50M valuation is not important.

Other firms have the opposite view and are strict on valuation because they believe it’s important to stay disciplined. Therefore, no matter how great your company is or how much they want to invest, they’ll bow out on valuation at a certain point.

What this means for founders: no matter how charming you are or how great your company is, some firms may not budge. It’s also admittedly hard to tell this from the outside. If possible, ask founder friends who have meaningfully engaged with them, or even better, someone who previously worked at the firm. You shouldn’t take any information you discover literally (there will always be exceptions), but it’ll help give insight into what might be possible, how much time to spend negotiating with a specific firm, etc.

Conclusion

The two best resources I read to navigate fundraising more were 1) the tech classic, Venture Deals by Brad Feld and 2) Never Split the Difference by Chris Voss (or watch the Masterclass - it’s great as well).

If you’re interested in this topic, I write weekly posts about things most helpful for founders - either things I have direct experience with (like this) or about things I’m actively researching and trying to solve myself. Future posts related to this include a) the most important terms to understand in a term sheet, b) how to answer “trick questions” from VCs like “how much are you raising” or “where are you in the fundraising process”, and c) the most effective way to build a network of VCs without a pre-established network. Subscribe here 🙏✨ and of course feel free to reach out if you have other questions, especially on Twitter.

Getting VC attention and term sheets is harder than ever, so congratulations for even being in the arena. And if you’ve made it this far in this post, thank you and I hope this becomes you:

<3,

Steph

About the author

Steph is the founder of PIN, a platform that handles all the back office legal/admin/tax work to enable groups of people (founders, company alum, accelerator cohorts, school alum, creators and their communities, etc) to invest together in startups. She created the first-ever inclusive investing club for her Stanford GSB class, which lead her to starting PIN to enable communities of all types to build their own clubs easily.

She was formerly a venture capital investor at NEA, where she invested in technology startups of all types from pre-seed through growth. She can be contacted via Twitter here.

Unlock the secrets to startup fundraising 🚀

Use our FREE, expert-backed playbook to define your valuation, build VC connections, and secure capital faster

Get my playbook

![12 Best Startup Financial Model Templates [Free & Paid]](https://d1pnnwteuly8z3.cloudfront.net/images/177302d9-3657-45b7-ac9d-acf801d83a74/1b029edf-43cf-4bd9-9e37-203f66bf426f.png)