Not a semester goes by without VC records being broken here in France and more broadly in Europe.

Glovo, TradeRepublic, Ledger… In S1 2021, French tech companies raised €5B (+90% YoY) while the German ones snagged €7.8B (+298% YoY), and the British ones €16B (+243% YoY). For everyone in tech, now is a good time to take VC money.

Yet, we see an opposite trend.

In France, more and more entrepreneurs chose to bootstrap and grow their business without external funding. Not one to shy away from a challenge, we now see VCs willing and adamant to invest in… bootstrapped companies.

The momentum for those atypical investments is high in France. Let's unpack it.

Table of Contents

What bootstrapping means in 2022

Let’s start where it all begins: entrepreneurs.

In 2022, bootstrapping is not a contingency plan anymore. Instead, many companies deliberately chose to grow without external financing and in spite of being courted by VC money. A couple of local examples: Lucca (HR software) and LeHibou (freelancing platform) are both well above €15M revenue, exhibit high growth, and yet are self-financed.

When asked about that choice, most founders give three reasons:

- Control: There is a general suspicion toward the VC space. Investors supposedly pressure companies to grow at all costs, leading to frequent financing rounds and unnecessary dilution. `Bootstrapped founders want to remain in control of their captable and management style.

- Agility: A bootstrapper can pivot and iterate far more easily than a VC-backed founder who “sold” her vision to investors, and therefore has a real or perceived obligation to execute on the agreed roadmap.

- Healthy corporate culture, not optimizing for VC “foie gras” growth: Where VC pushes for growth over profitability, bootstrappers hold profitability as the true cornerstone of a successful, sustainable startup. More broadly, bootstrappers rely on precise cash management: cash-in as soon as possible, keep an eye on all expenses and favour non-dilutive financing.

In the words of Charles Miglietti, CEO of Toucan Toco (data visualization), "Profitability was obvious to us, but a lot of startups are still starting to raise money without having validated their profitability!"

Bootstrapper needs financing... Wait, what?

OK, these founders want to stand on their own. If they are still around, they are probably doing something right. So why would they look for external funding?

Thibault Renouf, CEO of Partoo (online marketing), has bootstrapped for several years before accepting an €8M round in 2018:

"The question is never « should I choose bootstrapping or should I raise? » but rather « at which stage of the company deployment would external funding make more sense to accelerate?"

Launching a new product or entering a new geography may require more money than profitability and non-dilutive funding combined can provide. It was the case for Partoo in 2018, when they wanted `to break into the US market.

When this situation occurs, the management of a bootstrapped company has two options: either enter the VC game with rapid-paced fundraising, dilution, and hopefully hypergrowth, or raise funding only to reach a given milestone before returning to self-financing to avoid future dilution.

While most VCs are interested in nothing but the first option, we will focus on those who understand and look for the second option.

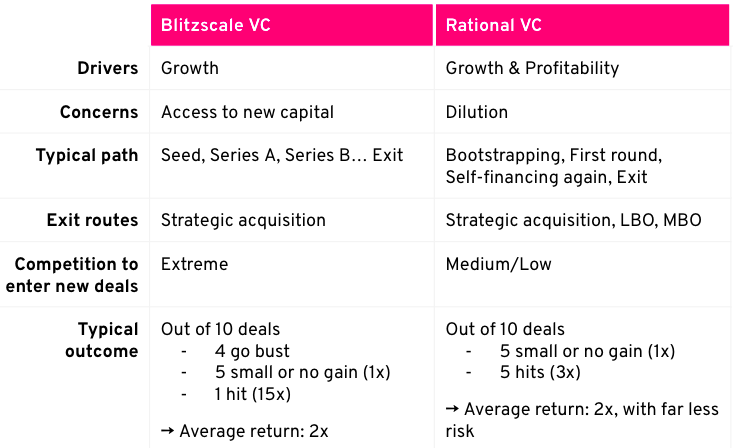

Rational VCs hunt for rational targets

Unlike "Blitzscale VCs", who evaluate companies with a growth-o-meter, “Rational VCs” search for both growth and profitability.

Those VC firms willing to invest in bootstrapped companies aren't part of a formal group, yet experience a strong momentum in France. Interinvest, Reflexion Capital, Tomcat Invest, Liberset have made it their core thesis and look at bootstrapped companies only. Others, like OneRagTime, combine both approaches.

In France, those players are three years old at most, which emphasizes how new this category of VC is.

In the US, the well-named Versatile VC invests in “capital-efficient” companies. It’s led by French-American VC David Teten. On their site, they write:

"At the most basic level, capital efficiency is a measure of whether a company uses its cash wisely. We don’t invest in either of the two most common forms of capital-inefficiency:

- A management team who focuses on raising as much VC as possible. This strategy makes sense for companies which fit the blitzscaling model, which typically means they operate in a winner-take-all market with network effects. But raising too much VC can cause serious damage or kill a promising company. Steve Cheney highlights that founders raising more money than they have a clear plan to spend tends to push them to spend unwisely. In a startup, a focus on doing fewer things well is imperative to winning.

- A management team which doesn’t understand how to think analytically about their financing and ownership options. By definition, such a team is not sophisticated enough to build an impactful company."

Another US player worth mentioning is Five Elms Capital. Their "anti-Valley" approach speaks for itself:

How do Rational VCs convince LPs?

Rational VCs reap off the benefits of their atypical investment thesis:

- Less dilution. Rational VCs benefit from the same advantages as bootstrapped founders: less dilution thanks to more negotiating leverage vs. future VCs.

- Less competition. As the segment is not serviced by existing funds, Rational VCs don't have to deal with today's intense competition between funds, which translates into more deal access and better terms.

- Lower initial valuation. Because many VCs have a bias against “lifestyle” founders, valuations are more reasonable.

- More resilience. Because of their financial discipline, bootstrapped founders have higher resilience to crises. Given we’re living through both a pandemic and a European land war in a two-year window, we all should be more aware of the risks of the unknown.

- More exit opportunities, ranging from big companies and LBO funds to management buyouts.

The last point is critical. Companies that keep this Rational style broaden the possibility of an exit after 3 to 5 years:

- From large corporations, which are better at valuing an acquisition on its EBITDA multiple rather than its ARR multiple, especially in France and in Europe.

- From LBO funds, which have not been so keen on tech so far, because structuring LBO on a non-profitable company is difficult by design. With Rational VCs portfolio, tech can be their new playground to deploy capital.

- From the company management themselves, for Management Buy-Out (MBO) is especially open for profitable companies. This is particularly the case for young management and/or those for whom independence was an important driver.

- While IPO can’t be ruled out, it remains the exception outside of biotech in France with less than 2% of total exits. Having said that, most IPO subscribers still want to see profitability around the corner.

Having more exit possibilities leads not only to better valuation, but also to an improved liquidity potential of Rational VC portfolios. This is a pivotal argument for Rational VCs to attract LPs.

Of course, Rational VC comes with its own issues. Beside traditional concerns on market potential, team focus..., the worst fear is to see your portfolio company turn into a Mom & Pop business, where growth is not a concern anymore.

Having said that, a "Rational portfolio" allows for exposure to tech innovation with less risk. An original and attractive proposition in these VC days.

The future of Rational VC

Most funds who position themselves as Rational VCs are young. Is this a temporary strategy before turning into a mainstream fund?

I think not. In fact, all the contrary: I expect a full cohort of Rational VCs focused on the topic.

First, because the euphoria in tech investment pushes risk averse LPs to choose Rational VCs over mainstream Blitzscale VCs.

Second, we are at the beginning of the ESG era, where S stands for social. A sustainable business model driven by profitability and longer-term thinking is what society calls for. Gone are the days when a company could raise a billion dollar, then carelessly fire 900 employees over a Zoom call.

Third, and more importantly, the number of companies choosing the bootstrapping path is on the rise. The newcomers benefit from the example of boostrapped companies created in the post-2008 crisis , when money was scarce, and who have now reached maturity. They also enjoy mature cloud infrastructure and no-code tools that drive down engineering costs, thus rendering venture funding less necessary.

In France, the shift is clear. The recent demise of NUMA and the Family, two major accelerators in France who championed the Blitzscale strategy and enjoyed huge media coverage in 2015 - 2019, feels like the end of a certain era.

Meanwhile, bootstrapped tech companies in France have formed the Club Bootstrap, which precisely aims at sharing good practice and bootstrapping culture among companies above €1M in revenue. The club already gathers 20+ members like Luko (insurance), Germinal (professional training) and Lemlist (leadgen).

To give you a taste of the mood in France, this was all over the headlines in 2021:

All players in the tech ecosystem, in France and abroad, should position themselves relatively to Rational VC and decide whether they want to be a part of it.

I hope this post serves as a first step to create awareness, understand founders' expectations, and ensure the alignment of Rational investing with your fund strategy.

Long live bootstrapping… and its financing!

About the author

Augustin de Cambourg is a founding partner at Shift Finance, an advisory boutique that offers end-to-end execution of fundraising and M&A operations for high-growth tech companies. Shift Finance has executed 20 deals for a combined value of €60M+.

Augustin can be reached at [email protected].

OpenVC is the best way to access deals 🤝

Browse the top 1% of deals and interact directly with founders. Completely free.

![12 Best Startup Financial Model Templates [Free & Paid]](https://d1pnnwteuly8z3.cloudfront.net/images/177302d9-3657-45b7-ac9d-acf801d83a74/1b029edf-43cf-4bd9-9e37-203f66bf426f.png)